People

- Adebiyi Fajemisin

- Anifat Ibrahim

- Raliat Sunmonu

Regions

Foreword

As the spread of COVID-19 first escalated to frightening levels, nations around the world took drastic action. Lockdowns and travel restrictions caught millions of small businesses off guard. Many shuttered their doors, while others were able to adapt to the circumstances. Globally, many are still recovering from the shock of the pandemic. Supply chain finance (SCF) is the use of financing mechanisms that can optimize the management of liquidity tied up in supply chain processes. SCF solutions have long been offered by big banks to large corporations, such as fast-moving consumer goods (FMCG) companies and manufacturers, to support trade.

Today, SCF techniques are being transformed by technology, expanding the addressable market to include micro, small, and medium size enterprises (MSMEs). Improved connectivity, increasingly available customer data, and new technologies lower the cost and make it possible to extend digital SCF solutions to the MSMEs at the end of global supply chains.

By tying credit to the flow of goods, SCF facilitates more efficient business operations and cash flow management for all actors along the chain — resulting in higher sales, faster turnover — and ultimately, increased profitability and growth.

A platform-based model that satisfies the interdependent needs of multiple stakeholders simultaneously using digital innovations is well suited to provide SCF solutions. Platform models consolidate digitized data produced by the flows of goods and money throughout the supply chain, building trust and facilitating coordinated decision-making. The net effect is to provide deeper insights into MSME and consumer behavior. Africa is at the forefront of many digital innovations for the underserved. We all have a lot to learn from what has been happening there.

In November 2018, the Mastercard Center for Inclusive Growth and Accion launched a partnership to transform millions of underserved MSMEs around the world and help them participate in, and benefit from, the digital economy.

Among other efforts, the partnership is reaching this goal by catalyzing the digital transformation of financial service providers and ecosystem participants. As evidenced in the Global Findex report released in June 2022, this work coincides with broad changes in customer behavior that have accelerated as a result of COVID-19.

Given the urgency of digital transformation to build an inclusive recovery, this paper provides timely insights into how to enable SCF models in three African countries and addresses key questions surrounding where to start and where to focus. Accion shares the insights gained from this work here, as part of our effort to ensure that our endeavors and accomplishments serve as demonstration models for the industry.

Prateek Shrivastava

Vice President, Digital, Accion Global Advisory Solutions

Executive summary

The global pandemic and attendant economic crises painted in stark relief the dire reality of what exclusion from the digital economy truly means for Africa’s small-scale merchants. As lockdowns restricted access to customers and suppliers alike, disrupted supply chains led to empty shelves and small business owners saw both formal and informal channels for funding dry up, exacerbating persistent access to capital challenges. Adopting digitally enabled solutions to buy, run, and sell better became an imperative for the survival of the micro, small, and medium businesses (MSMEs) that make up 90 percent of businesses and create 80 percent of jobs on the continent.

For MSMEs in particular, the pandemic has catalyzed a proliferation and expansion of platform-enabled, tailored supply chain solutions. Emerging players such as Boost, OmniBiz, and Wasoko may have different models, but all have a common goal: to simplify traditional supply chain flows and solve persistent credit, distribution, and productivity challenges small African merchants face.

Supply chain finance (SCF) solutions aim to leverage relationships and data flows between actors in the supply chain ecosystem to offer high-quality, low(er)-risk financing to actors in the ecosystem. Building on our previous work that explored how digitized supply chains can help small businesses grow, Accion undertook a study in three key African markets to identify opportunities for enhancing and scaling digitally enabled supply chain finance solutions to accelerate growth of MSME merchants.

To better understand market-specific factors and macro systemic influences, Accion selected three countries in Africa that have embarked on similar digital financial inclusion journeys, but are at different stages of maturity on the digital transformation continuum: Ghana, Ethiopia, and Nigeria. A common trend in supply chain ecosystems across all three countries was the emergence (nascent in Ethiopia’s case) of merchant-centric, platform-led fintechs and other players complementing, or in some cases, competing with, traditional distributors to leverage supply chain relationships, data, and digital technologies to address inefficiencies in inventory, logistics, credit, and collections typically seen in traditional models. These players are building supply chain solutions centered around small merchants, incorporating solutions that go beyond access to credit to include various other services such as inventory management, market intelligence, and logistics support.

While these models will continue to coexist and even play complementary roles in any one market, the core building blocks for any successful and ultimately sustainable model must include:

- An integrated, omni-channel approach to merchant recruitment, engagement, and support: Ecosystem actors deploy multiple various channels and personnel, from field agents used by platform providers to banks’ account officers to FMCG company or distributor agents who deliver stock and provide other support. There is plenty of opportunity to engage, or sometimes confuse, merchants. A well-designed merchant engagement and support strategy that is explicit about the responsibilities of each ecosystem partner and provides a smooth customer experience despite inherent complexities is critical, but one of the more challenging things to get right.

- Multi-faceted approach to convert cash transactions to digital payment mechanisms: Despite great strides in the digital payments space, particularly in Ghana and Nigeria, cash transactions continue to account for 90 percent of all transactions. Regulations such as Ghana’s 1.5 percent levy on digital payments don’t help. While partnerships with providers such as mobile money operators, agency banking networks, and international card schemes will continue to be key, accelerating conversion to digital payments requires helping merchants not only use, but also accept, digital payment instruments from their own customers.

- Willingness by partner banks to offer credit: The key to a successful deployment of supply chain finance is the willingness of financial services providers (FSPs) to offer credit products to MSMEs based on supply chain data, which is something FSPs may not be comfortable with. This risk can be mitigated by working with credit guarantee providers. Once the FSP is able to move forward, it then needs to plan for the need for increased liquidity due to the fresh demand coming via the SCF products. The cost of debt finance for on-lending if denominated in foreign currency and limited options for credit risk guarantees creates a barrier, with potentially prohibitive costs to the FSP.

- Enhancing value-added services to promote merchant “stickiness”: One key finding was that while uptake of various supply chain solutions has seen exponential growth in the target markets, the ratio of active merchants over time as a percentage of the overall customer base was much more modest. This suggests that long-term adoption by merchants depends on improvements to how they run their businesses and buy and sell goods — with demonstrable benefits to their bottom line and ease of doing business.

There is clearly an appetite from financial institutions, FMCG companies, and other service providers to offer MSMEs SCF solutions sustainably and profitably. However, despite great strides made by new and emerging players in the space, there is a long way to go and plenty of opportunity for non-supply chain actors to accelerate the gains:

- Catalytic funding for innovation: Development finance institutions (DFIs) and similar institutions can provide funding in the form of credit guarantee schemes, grants, low-interest loans, and similar catalytic funding to grow demonstration models, provide risk mitigation to commercial lenders, and provide long(er) runways to nascent startups.

- Accessible global expertise for local deployment: International consulting and advisory firms with particular expertise in serving small-scale merchants can make niche subject matter expertise and global learnings available locally, thus helping to cross-pollinate ideas, leverage learnings from other markets, and spur innovation. Expertise can be deployed to position SCF solutions more acutely to better serve target customer sub-segments with specific needs, such as women or young entrepreneurs.

- Better capacity building and collaboration among players: International actors like FMCG companies or FSPs that have embarked on various demonstration models across Africa and other regions can share the lessons they have learned and provide capacity building to others looking to build or scale their own supply chain finance models. Regarding collaboration, international payment schemes can provide bespoke solutions to acquirers and issuers that are more affordable, simpler, and easier to adopt by merchants. This will help facilitate better adoption of digital payments throughout the value chain.

Introduction

Much has been said about African micro, small, and medium businesses’ criticality to the continent’s survival and growth, and the barriers they face — chiefly access to affordable credit, markets, and business support services. Governments, in partnership with the private sector, have initiated various regulatory, macroeconomic, and structural reforms to address these challenges and spur growth as part of sweeping national financial inclusion strategies. Though countries are at various stages of implementation of these strategies, and the environmental, political, and infrastructural readiness differs, from Morocco to Mozambique, Ghana to Ethiopia, and countries between, there is a focus on exploring opportunities to leverage digitization and digital tools to create scale and find new ways of solving old-age challenges.

With support from Mastercard’s Center for Inclusive Growth and as part of a broader global initiative to impact the lives of 10 million people through digital transformation of their financial services providers and enable 4 million MSMEs to run, buy and sell better, Accion undertook a project in three African markets to explore the opportunities to better serve MSMEs in the fastmoving consumer goods (FMCG) retail sector, through access to more reliable working capital and other services.

MSMEs contribute significantly to the revenues of large FMCG companies and in recent years, new digital-first players have emerged, many focused on helping MSMEs accelerate the digitization of their business and crucial financing, market insights, and business support services. These new players are changing the supply chain landscape, creating new models that enhance or replace existing structures and, in the process, helping MSMEs leapfrog perennial challenges and recover and rebuild from the pandemic. Women, for whom traditional models pose even more barriers when it comes to finance and market access, can benefit greatly from these new approaches.

Accion selected three of sub-Saharan Africa’s most promising markets for MSME-led digital financial inclusion: Ethiopia, Ghana, and Nigeria. Accion’s activities were focused on the following: a) understanding the general supply chain landscape, country-specific challenges, pain points, and opportunities for addressing latent or unmet needs of key actors; b) identifying context-specific key building blocks for successfully offering and expanding supply chain financing for small and micro retailers, as well as exploring trade-offs and key success factors; and c) providing pragmatic, actionable recommendations for implementation and the role of third parties in the SCF ecosystem. This market research builds on our previous work, The Supply Chain Finance Opportunity, that explored how digitized supply chains can help small businesses grow.

Country profiles

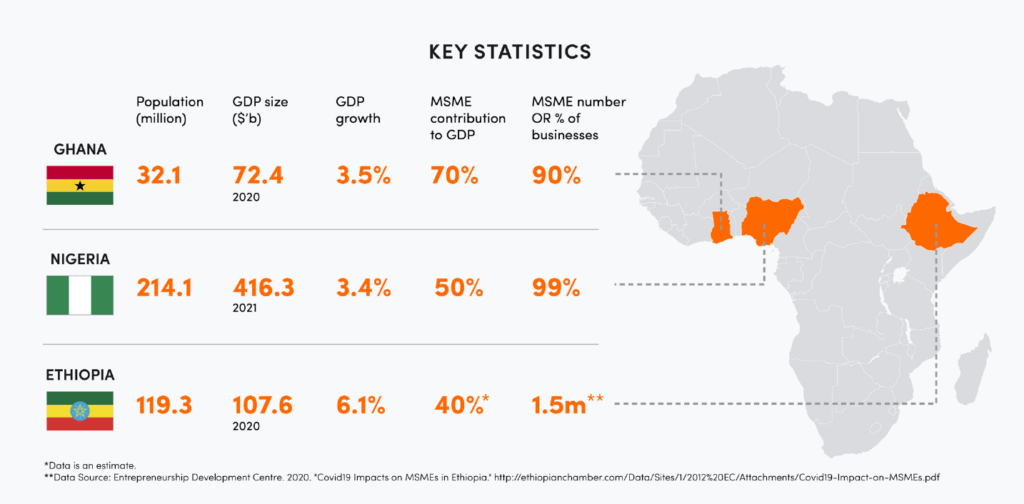

Ghana is a small country in West Africa with a population of approximately 32 million people, but it is one of Africa’s fastest growing economies. An economy described as “skyrocketing,” the International Monetary Fund (IMF) in its World Economic Outlook predicted that Ghana’s economy would be the fastest-growing economy in 2019, with a GDP of 8.8 percent. Although Ghana’s economic growth was halted by the COVID-19 pandemic more recently, the World Bank estimates the growth to have reached 4.1 percent in 2021 and is projected to reach 5.5 percent in 2022. Ghana enjoys economic and political stability, providing a conducive environment for conducting business. MSMEs play a significant role in Ghana, accounting for more than 80 percent of employment (versus 67 percent globally) and over 70 percent of private-sector output

(versus 52 percent globally).

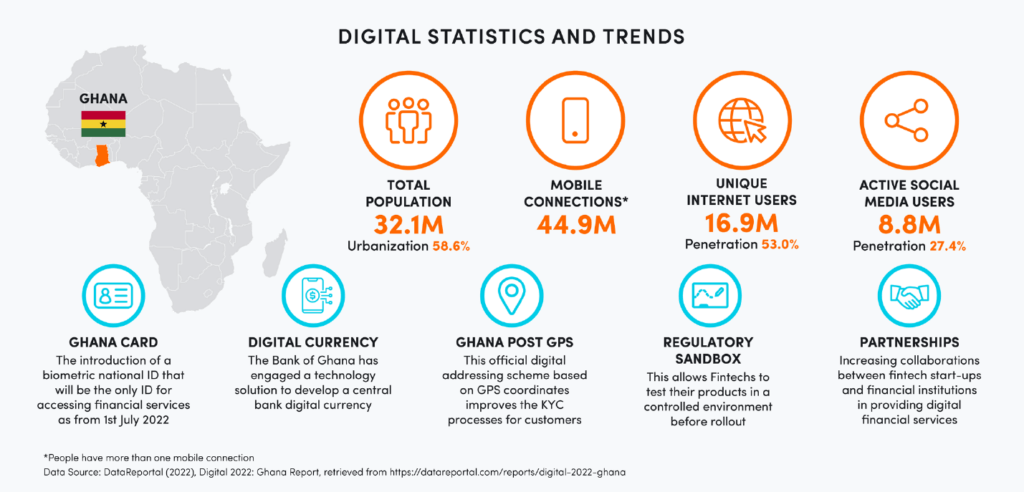

Ghana is an innovation leader known to have launched the world’s first digital financial services (DFS) policy and the first African country to launch the interoperable payment acceptance solution known as universal QR codes. The government is driving the digital transformation of the economy with key enablers such as the Ghana Card, digital address system, mobile money interoperability, universal QR codes, and Ghana.gov platform as drivers of economic growth. In 2020, Ghana launched three policies to deepen financial inclusion and accelerate the shift to digital payments: the National Financial Inclusion and Development Strategy (NFIDS), the Digital Financial Services (DFS) policy, and the Cash-Lite Roadmap. There are over 70 unique fintech services in Ghana offering specialized services to individuals, businesses, and the government. The Bank of Ghana, the key regulator of financial services in the country, established the FinTech and Innovation Office, providing guidelines for permissible activities for electronic money issuers and payment service providers.

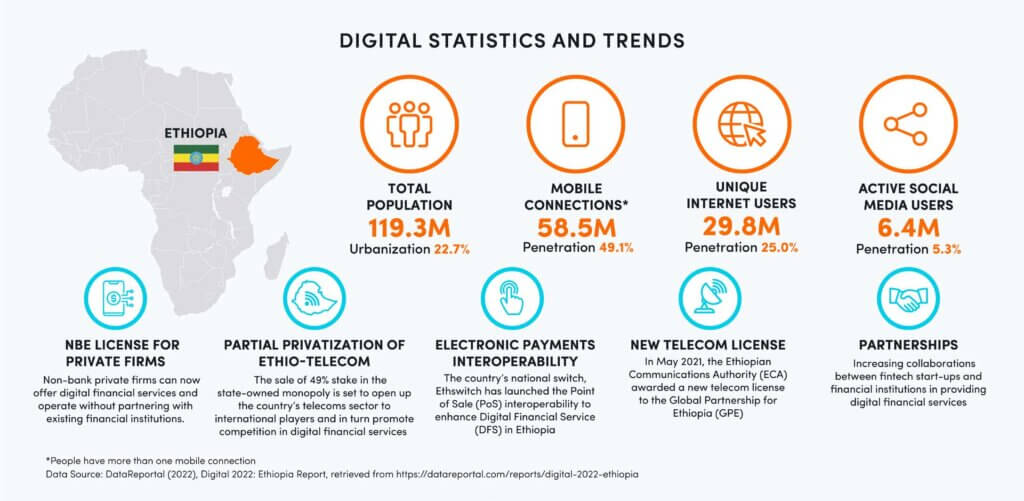

With about 119.3 million people in 2022, Ethiopia is the second-most populous nation in Africa after Nigeria. With a per capita gross national income of $890, it is also one of the poorest countries in the world. Even though the country has a high poverty rate, the World Bank reports that Ethiopia has been one of the fastest-growing economies in the last 15 years. Ethiopia has an estimated 1.5 million MSMEs10 that plays a significant role in the economy employing up to 4.5 million people before the Covid-19 partial lockdown. With Ethiopia being a country with low private enterprises per capita, it is important to support the MSMEs by filling the finance gap and putting in place favourable economic policies to allow these businesses to thrive.

Currently, the Ethiopian government’s socioeconomic mission focuses on transforming the country into a middle-income country by 2025. Industrialization has been prioritized as the main driver of economic growth and job creation. The government launched a 10-year development plan that will facilitate a shift to a private sector-led economy by introducing competition growth-enabling sectors (energy, logistics, and telecom) and improving the general business climate.

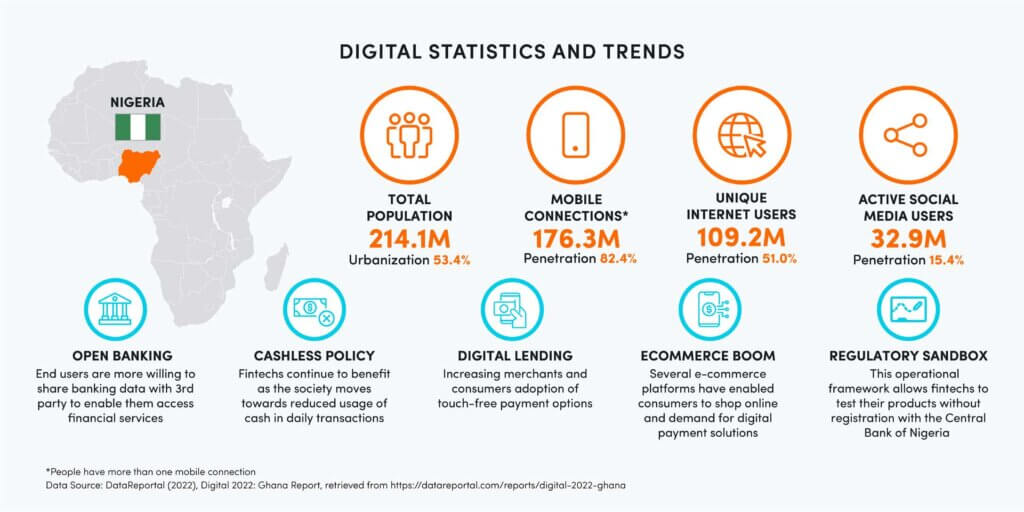

Nigeria’s economy is the largest of any country in Africa, accounting for about half of West Africa’s population with approximately 214 million people. Nigeria is a middle-income, mixed economy with expanding prospects in the manufacturing, financial services, technology, and entertainment sectors. Nigeria also boasts one of the most successful startup ecosystems on the continent, securing 42 percent of the continent’s capital inflows in 2021 and three unicorns (companies valued at $1 billion or more). A large proportion of these startups are fintechs focused on digital banking, lending, and digital payments.

Microbusinesses make up 99.8 percent of Nigeria’s MSME sector, businesses that are mostly unregistered, informal, and largely unable to fully participate in the thriving digital economy.

In this report, we share learnings and provide insights on how actors can collaborate to enable more small and micro merchants to access reliable finance, better manage their businesses, and grow. The report outlines common supply chain finance models in the target countries and, while recognizing that there isn’t one model that fits all needs, we have also explored the key building blocks for any sustainable, scalable model and offer practical guidelines for implementation for various actors. We hope that this report is helpful to supply chain actors (e.g., financial institutions, logistics providers, digital platforms), and the wider ecosystem as they chart a path to accelerate the recovery, resilience, and growth of millions of micro and small merchants.

Part 1: FMCG supply chain in Ghana, Ethiopia and Nigeria

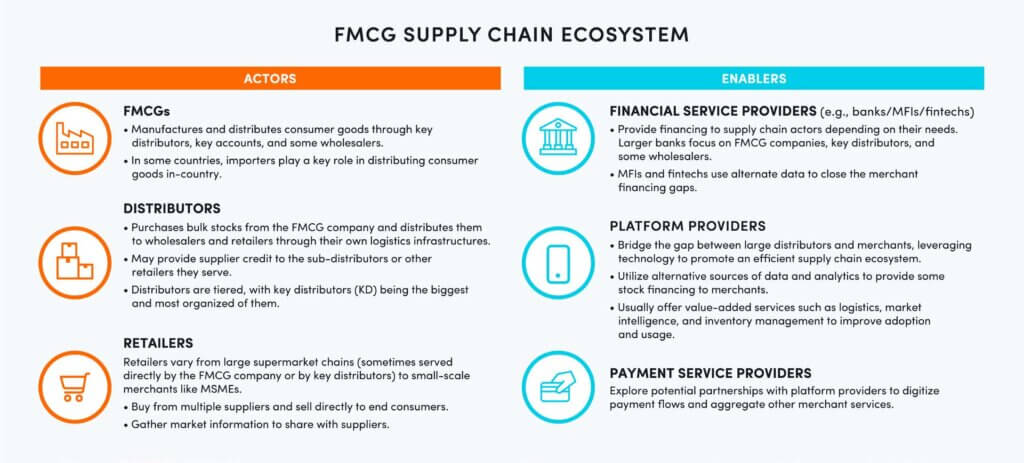

The FMCG supply chain ecosystem comprises a network of cross-industry actors that play unique roles in moving goods from the manufacturers to the final consumers. The operations within the supply chain ecosystem of Ghana, Ethiopia, and Nigeria being considered in this report are similar, with just a few differences, especially in Ethiopia. All the three countries have local and international players (FMCG companies, financial service providers (FSPs), distributors, and retailers) that make up the traditional supply chain model, as well as emerging players such as the platform providers.

The roles of each of the actors can be summarized as follows:

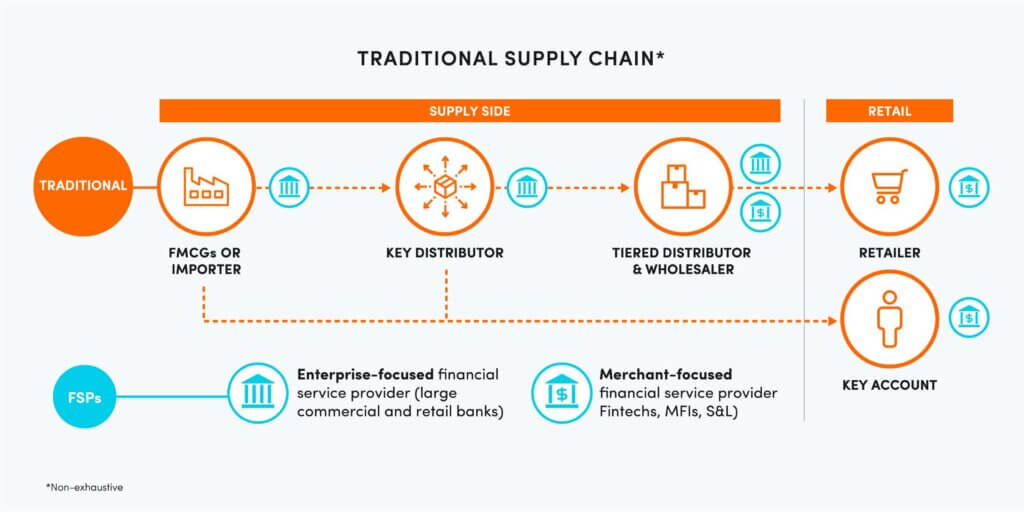

In the traditional supply chain model, the flow of goods starts from the FMCG company or importer and passes through several distribution layers before getting to the last-mile retailer, often an MSME. This model presents several challenges to the MSME, as well as the other actors in the chain.

Inefficiencies and lack of support for MSMEs in particular within traditional supply chains make it difficult for them to scale their businesses, irrespective of how long they have been in operation.

Abdurahaman Sadik is a second-generation retail shop merchant in Addis Ababa, Ethiopia. The business was started by his father and uncle 15 years ago in the same small shop. He sells soft drinks, bottled water, confectionaries, and home and personal care products. Abdurahaman started running the business alone in the last two years and still faces the same challenges that hindered the growth of the business since its inception.

Running a retail shop is tough for small merchants like Abdurahaman, no matter how long they have been in business. Restocking Abdurahaman’s shop is stressful, expensive, and time-consuming. He closes his shop for half a day to go and buy goods from wholesalers at the open market. These wholesalers sell goods to him at high prices, leaving him with a small profit margin. Beyond this, he incurs additional costs such as transportation and loading and offloading goods that further reduce his already low margins.

Abdurahaman remarked that optimizing working capital and maintaining steady cash flow is hard, because most suppliers do not offer credit, while many of his customers buy products on credit and pay later. Like many MSMEs, Abdurahaman experiences difficulties in obtaining loans from FSPs. According to him, FSPs are typically unwilling to offer loans to small merchants like him. They demand collateral and other requirements that are hard to fulfill, have complicated processes that are time-consuming with a high opportunity cost for a sole entrepreneur, and take so long to turn around that even if the loan is approved, it misses the merchant’s critical need window. Of course, to FSPs and other traditional lenders, merchants like Abdurrahman who only keep handwritten sales records (if at all), have low digital literacy skills, and rarely separate business and personal finance, are high risk and expensive to serve.

Many actors in the supply chain ecosystem lack the visibility to understand and access data pertaining to the business operations of merchants at the end of the chain; for example, in order to optimize operational efficiencies, FMCG companies’ route to market typically relies on select “key distributors” (KDs), sub-distributors, and large retailers to handle sales, support, and order fulfillment for smaller merchants. This lack of visibility of the last-mile operations reduces their ability to support and empower lower chain actors.

Key distributors are not well positioned to support small merchants either. Their business models are often dictated by the FMCG companies, frequently with little opportunity or motivation to deepen relationships with small merchants beyond their sales and order fulfillment remit, leading to a largely transactional relationship with merchants. While wholesalers are much closer to the small retailers, they lack the capacity, systems, and operational efficiencies — many of them engage in manual bookkeeping, ordering, and inventory management processes — to act as effective bridges between the larger players and the merchant.

Small merchants like Abdurahaman are eager to grow and capitalize on new business opportunities and to do so, they need to change their business practices and embrace digitally enabled solutions that will position them to access new sources of credit and customers and to grow. Changing how they operate their businesses means changing how the ecosystem collaborates and operates.

Newer, more disruptive models that are platform-enabled have emerged, centered around MSMEs. These platform providers help retailers overcome several challenges, including inconsistent inventory availability, logistics and transportation issues, limited access to financial services, and unreliable market pricing trends. This model is similar in operations to the traditional supply chain, but leverages technology to bring merchants online, many for the first time, and serve as a broker between them and the distribution chain. By digitizing the supply chain through the emerging platforms, retailers can order goods at their own convenience and have access to additional services that can help scale up their businesses. Specifically, platform providers offer factory-to-retail distribution of FMCG goods, digitize the chain from distributors to retailers, and provide additional technology-driven value-added services for small and micro merchants. They may provide logistics services to merchants directly or via partnerships with independent logistics providers. Platform providers also utilize data generated on their systems to assess the creditworthiness of merchants and use this to provide different forms of stock financing on- or off-balance sheet.

These platform players are fast growing in Nigeria and Ghana, with many having all emerged in the last five years. The situation is different in Ethiopia, where regulatory and weak infrastructure for DFS have until recently constrained the emergence of digital lending solutions and adjacent services.

The rise of platform players in Ghana and Nigeria

Ghana and Nigeria in particular have witnessed a rise in the number and types of platform-enabled SCF solution providers for MSMEs. Examples are Boost and Shopa in Ghana and Innovectives, Omnibiz, and Tradedpot operating in Nigeria, with each of them providing different forms of stock financing on- or off-balance sheet.

Part 2: The changing landscape of supply chain finance

Traditionally, access to credit within the supply chain was focused on the larger players, provided by the supplier, an FSP, the FMCG company itself, and, more recently, fintechs. Typically, FSPs are enterprise-focused and tend to serve FMCG companies and larger players (e.g., importers, key distributors, and wholesalers), offering access to credit in the form of working capital loans, asset financing, and invoice discounting, often requiring collateral or other forms of guarantees. Even FSPs such as microfinance institutions that serve smaller actors such as wholesalers and MSMEs also require collateral and guarantees from these customers.

Running a scalable retail business can be very challenging for small and micro merchants with limited or no access to business finance. According to the International Finance Corporation, the funding gap for MSMEs amounts to $5.2 trillion every year, leaving many small and micro merchants to often rely on informal means to expand their business operations and meet the needs of consumers. Merchants typically have fluctuations in sales, but they often experience higher than normal sales at certain periods of the year, like festive seasons, leaving them determined to have more stock in their shops to meet demand. Unfortunately, many do not have the financial resources to either increase stock, improve product variety, or introduce brands that are in demand. In an ideal situation, these merchants should be able to apply for business loans from financial institutions, but this is not the case, as this segment is often considered unattractive and high risk to financial services providers. They should also be able to approach distributors to sell products to them on credit, but distributors only sell goods on credit to a tiny percentage of merchants, often based on long-term tested and trusted business relationships and other externalities. Exacerbating the situation is the fact that merchants have heavily manual operations which barely generate data that can showcase their financial positions or help them build credit profiles.

Supply chain finance (SCF) solutions aim to leverage relationships and data flows between actors in the supply chain ecosystem to offer high-quality, low(er)-risk financing to actors in the ecosystem. Supply chain finance is different from traditional lending in that the funder (lender) pays the supplier in advance, uses the buyer’s stock as security for the credit facility, and utilizes the data from what is supplied and purchased to optimize the lending agreement.

Providing merchants at the end of the retail chain with financing requires significant digitization of processes and data. This level of digitization means that the finance arrangement needs to be supported by the right technology, which allows actors to consolidate and share real-time data produced by the movement of money and goods in the supply chain to facilitate coordinated decision-making and enable retailer financing. This requires bringing small and micro merchants online (some for the first time) and working with them through a sustained and evolutionary journey of digitizing key aspects of the business, from stock ordering to inventory management and payment services.

Extending financing and other services to small-scale merchants in the FMCG supply chain is a win-win proposition for all actors in the value chain. Beyond the short-term benefit of providing reliable working capital to merchants who typically are unable to get it affordably because they lack collateral, guarantees, and other requirements, it also helps merchants build stronger business credit profiles, improve their relationships with their suppliers (distributors), enable them to have more stable cash flows, and help them remain focused on their personal and business goals. Because many micro and small businesses often mix business and personal finance, supply chain finance gives them a clearer picture of their business obligations. For distributors, SCF enables them to better control their cash flow, have faster access to payments, and build stronger relationships with their downline merchants.

Traditional supply chain financing model

The traditional supply chain financing model is not new, especially in the FMCG supply chain ecosystem. Still, its focus has been on the bigger players, such as key distributors, tiered distributors, and key accounts backed by the FMCG companies. In this arrangement, the FMCG company plays a key role in providing some form of guarantee with the overall objective of easing financing and cash flows between the FMCG company and those it directly interacts with.

Beyond this, there is occasional supply chain financing between the distributor and merchants, with the former offering goods on credit options. In many cases, this arrangement is not formalized or guaranteed and is based on personal relationships between the distributor and the merchant.

Given its nature and structure, it poses several limitations as funding is accessible by only a select group of actors (key distributors, tiered distributors, and key accounts), while small and micro merchants are typically excluded and therefore not able to benefit despite being a key contributor to sales and the entire ecosystem.

Emerging supply chain financing models

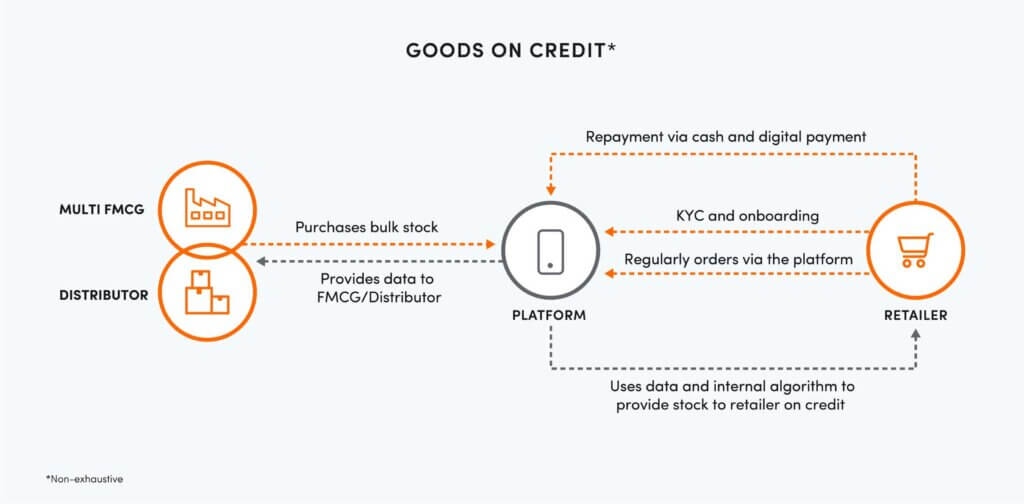

The platform-enabled financing archetypes within Nigeria and Ghana are primarily of two types: Goods on credit model and the FSP partnership model.

In the Goods on credit model, the platform provider finances stock on its balance sheet and bears the full risk. It is responsible for know your customer (KYC) verification, actively managing onboarding and customer relationships through agents who are deployed on the ground. It utilizes merchant data generated through the platform and, using data analytics and artificial intelligence, assesses and determines the credit score and amounts per qualifying merchant. Platform providers typically start with this model and progress to either forming partnerships or sourcing on-lending options as demand for credit goes beyond what their balance sheet can administer. Example of players using this model are Boost in Ghana and TradeDepot and Omnibiz in Nigeria.

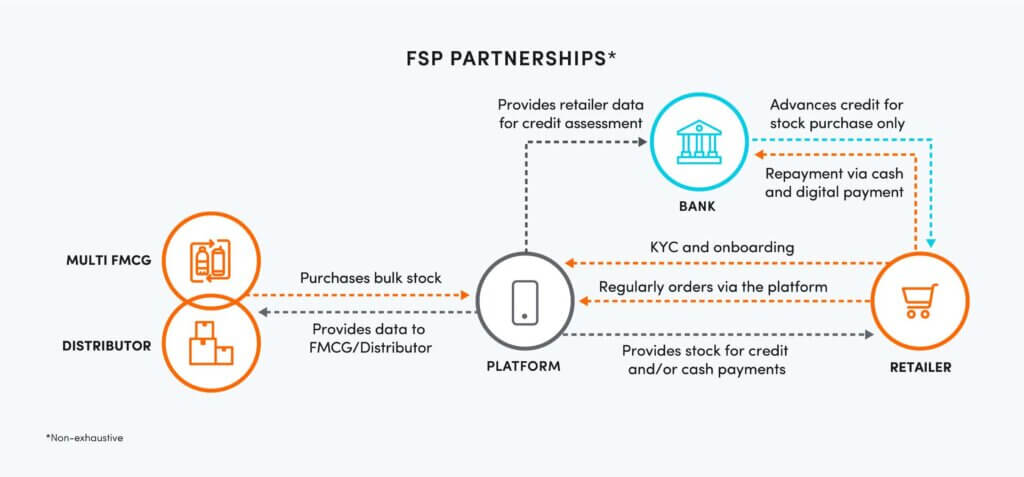

The FSP partnership model is like the Goods on credit model, but in this instance, an MSME-focused FSP is introduced to take on the risk. However, in some cases, the platform may provide a first loss guarantee to the FSP in return for a revenue share with the FSP. Platform providers partner with an FSP to provide credit directly to retailers to purchase stock, utilizing merchant data to pre-score merchants and then passing this credit scoring information to its partner FSP. It actively manages onboarding and KYC verification and has agents deployed to actively manage customer relationships and issue resolution. Although considered a better model as it doesn’t put pressure on the platform’s balance sheet, platform providers have struggled to partner with mainstream banks due to risk-sharing requirements. Examples are Shopa and Pezesha in Ghana and Innovectives and Cowries Microfinance Bank in Nigeria.

Though both the Goods on credit and the FSP partnership models appear similar across most operational areas, there are a few differences in how credit decisions are made and disbursed; though to the merchant, there is little functional difference. In the former, the platform provides credit in the form of goods to the retailers, usually for a period of up to three weeks, whereas in the FSP partnership model, the third-party lender provides credit to purchase stock for the retailers with repayment agreements in place.

The platform-enabled SCF has tackled some of the issues of the traditional SCF, but they are not without their challenges. Apart from the models slowly gaining traction in Nigeria and Ghana, these two models face much deeper structural and economic challenges that threaten their scalability. Many small and micro merchants being served have low digital literacy skills, and there continues to be a heavy reliance on field agents to support customer onboarding, proactive engagement, and support. Many platform providers have also switched from native apps to WhatsApp bots in order to be able to serve these merchants.

Converting cash to digital continues to be challenging. Although several attempts have been made to integrate various options, these have not generated the desired effect because the focus has been on the merchant payment requirements, without involving the end consumer and their suppliers.

Under these models, platform providers may also need to bear additional logistics costs of delivering goods to the last-mile retailer, as the distributor with which they have existing relationships may be unable to fulfill orders when demand is high.

The introduction of platform-enabled supply chain models has provided the opportunity to rethink how supply chain finance for the lower end of the retail chain can be done. Platform providers have continued to explore different methodologies and approaches with varying degrees of success, but it is clear that they are beginning to reach into and address some of the key pain points of small and micro merchants. While there has been progress, there are a few pertinent factors that platform-enabled participants need to consider in building and scaling their models, which are addressed in subsequent sections of this report.

Part 3: Approach to building and scaling supply chain financing

Implementing a platform-enabled model for offering working capital and other services to small merchants can address key barriers that have historically led to the exclusion of many merchants from the formal financial system. The various solutions we’ve seen in the three markets have employed varying business models and approaches to solve key pain points for their target demographics. Our review of these various models and learnings from implementations in other markets, such as Jaza Duka in Kenya, suggest that six factors in particular significantly contribute to the success of an MSME-centered supply chain finance model.

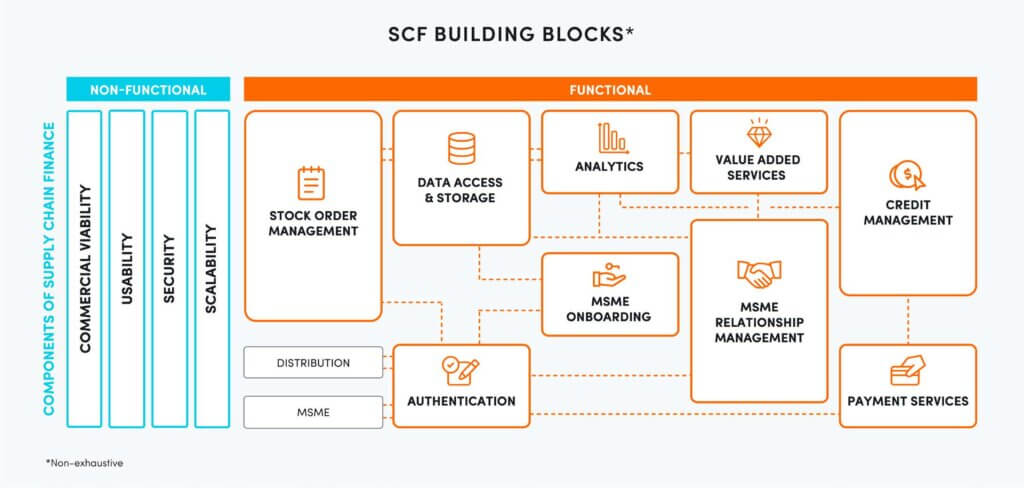

1. Build the right foundation (SCF building blocks)

The success of a fully integrated supply chain financing model requires that several components need to be considered by actors in the supply chain and FSPs. From our research, we have identified some base components which cut across functional and non-functional considerations and form the broad requirements that would be needed to satisfy a platform-enabled SCF model.

Actors should consider the following functional issues when building or scaling a platform-enabled SCF model for small and micro merchants:

Onboarding: What are the minimum requirements for KYC, and how can this be fulfilled in a cost-effective manner while meeting regulatory requirements? What is the minimum data required to onboard? What is the right combination of digital and in-person channels that best meets the target market?

Stock order management: How and where should retailers order their stock, and how can the data be maximized for analytics and credit assessment? What are the stock fulfillment processes and roles of relevant actors? What integration is required between distributors and FMCG companies? How should logistics be addressed — internally, outsourced, or both?

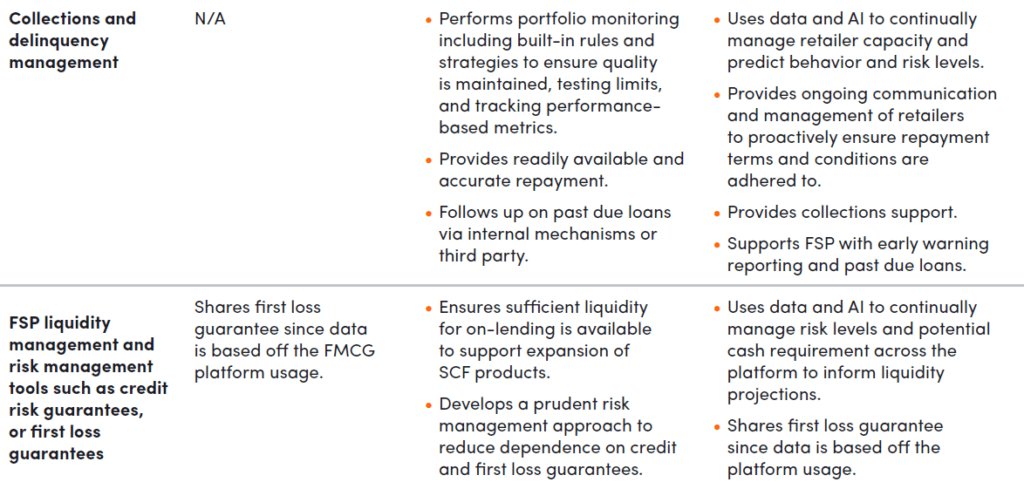

Credit management: What additional KYC is required to complete the loan account opening processes, and how should these be sourced? How will credit scoring be performed, and what are the distinguishing roles of the platform and lenders? How will credit be accepted by the merchant and disbursed when credit purchases are initiated? What are the distinguishing roles of the platform and lenders in collections and managing delinquencies?

Relationship management: What is the customer management strategy and approach? What is the right combination of self-service and in-person channels to manage the customer? What ongoing support structures will be provided to ensure proper handholding and effective issue resolution?

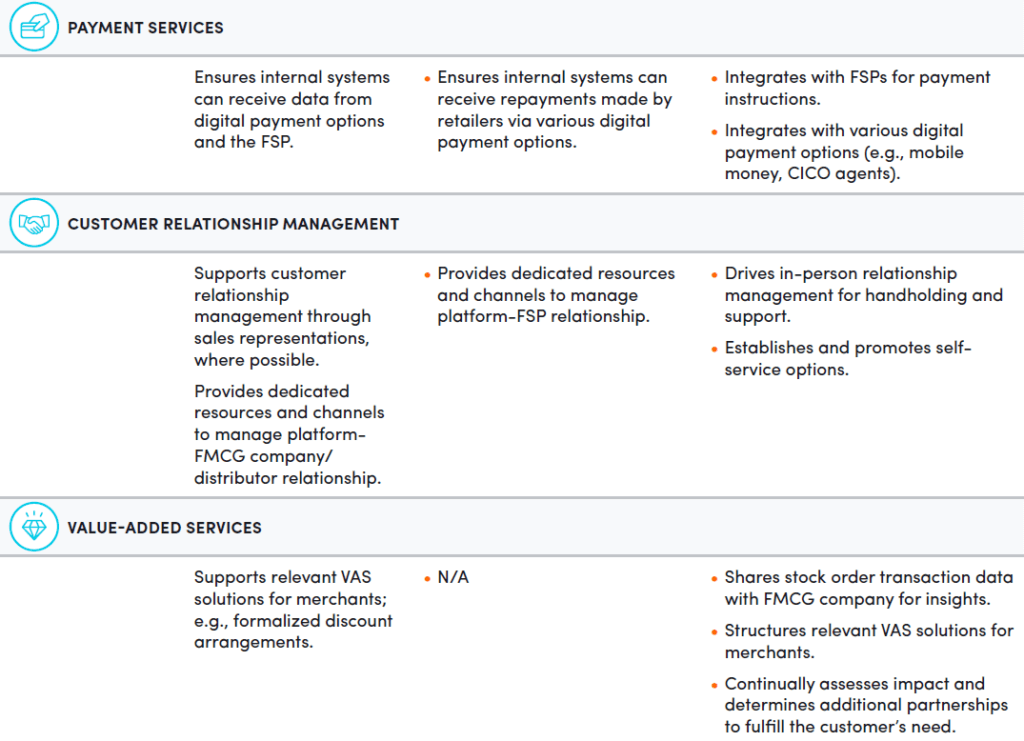

Payment services: What are the relevant digital payment services available to merchants, and how can these be integrated into the platform to drive digital payment adoption? Are there incentives that can be provided to ensure merchants shift from cash to digital payments?

Value-added services: What specific value-added services, such as market intelligence, financial literacy, and business capacity building, would be relevant to the target market, and how can these be incorporated into the model? What is the most effective financial model that will ensure value-added services remain viable?

Authentication: How should distributors and merchants be authenticated to ensure safety and minimize fraud during transactions?

Data access and storage: How and where should merchant KYC and transaction data be securely stored? Are there regulatory limitations on where data can be stored? What are existing/planned data privacy laws and their implication for data collection processes and data sharing among actors?

Analytics: What is the data analytics rules engine? What are the dashboard requirements across actors? How can data be leveraged to provide market intelligence across participants?

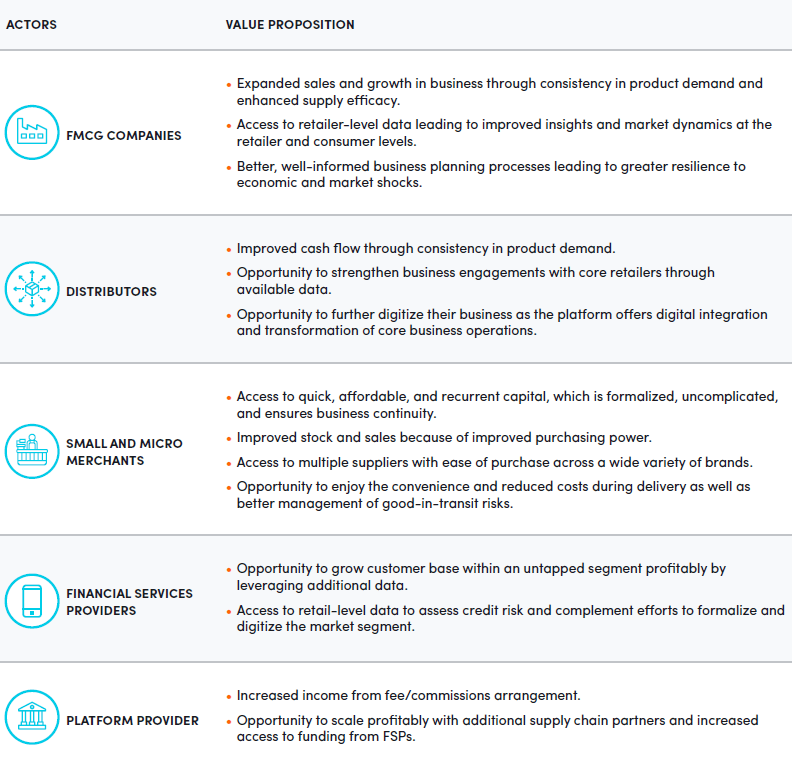

2. Get the value proposition right

Realizing and accruing the potential benefits, as shown below, requires careful orchestration and effective collaboration among these ecosystem parties. In platform-enabled models, this orchestrator/facilitator role is often undertaken — by design or happenstance — by the platform provider, but it can be taken on by any of the service providers in the chain (e.g., FMCG companies or FSPs). The success of the enterprise relies in part on the alignment of interests and the skill of the facilitator entity in managing disparate interests to serve a common goal.

3. Adopt a multi-partnership approach

Merchants source their goods from various suppliers and even in the open market to ensure they can provide the product variety their customers require. Therefore, it is essential to partner and integrate into multiple sources of stock (multiple FMCG companies and their distributors) and sources of funding (multiple FSPs), so merchants have a “one-stop-shop” access to most of their stock requirements and the additional funding that may be required to purchase them.

Platform providers either provide lending on balance sheets or drive a FSP partnership. While we have established that the former is restrictive based on the risk they can take on their balance sheet, most FSP partnerships have also been with smaller MFIs and fintechs, again limiting the extent to which credit can be provided. Mainstream commercial banks have deep pockets and could easily drive lending scale in these models, but they are reluctant as they see small and micro merchants as very risky with a high cost to acquire and serve.

Nonetheless, platform providers need to drive multiple partnerships with these large banks but work to address their credit risk concerns. Large FSPs have historically used static data (financial statements) and sometimes bank account history to assess MSMEs, requesting for guarantees and collateral to further mitigate their risk and protect their capital. The platform provider can demonstrate that the use of alternative data such as order history, sales history, and payment transaction history can enhance the assessment of a merchant’s creditworthiness with resultant low levels of credit losses. Platform providers can also showcase their customer acquisition and management approaches and work with the FSPs to explore a mix of strategies that will translate these relationship management approaches to better collection mechanisms and ensuring delinquencies can be kept to a minimum.

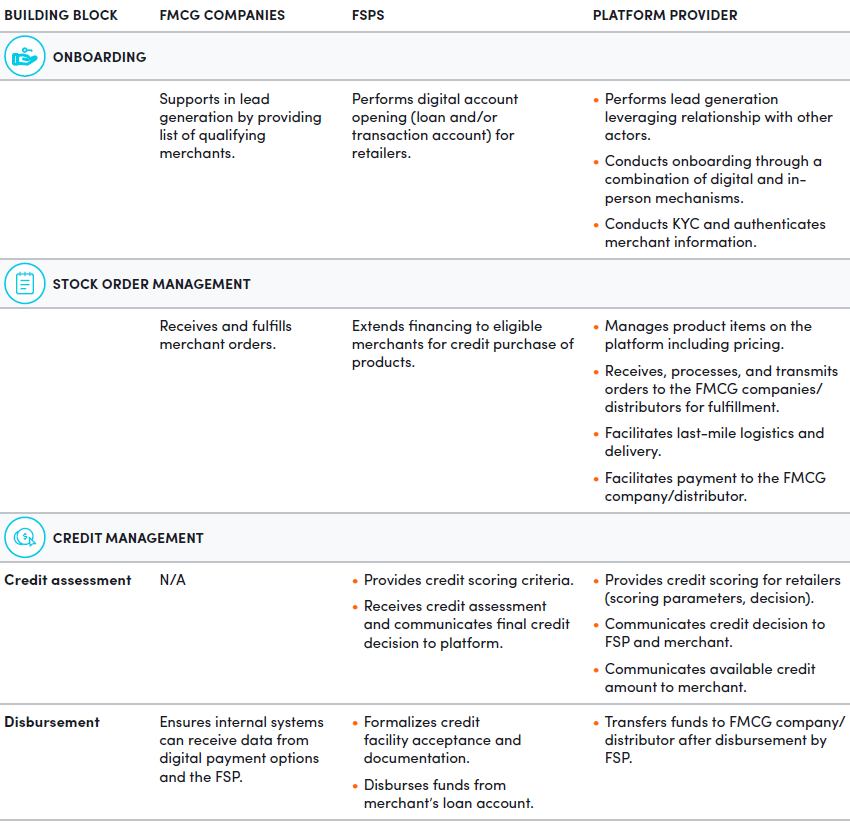

4. Clearly define the key roles of actors within the SCF ecosystem

Poorly defined roles within an ecosystem create a lack of clarity, overlap in activities, and long-term inefficiencies. It is therefore important that all actors are clear and fully aligned on what roles they play within the SCF ecosystems. Based on our research and experience, we have suggested below some critical roles along key elements of the building blocks for FMCG companies, FSPs, and the platform provider. While these roles are not exhaustive, they do provide a foundational basis by which actors can discuss and agree.

5. Understand the levers that underpin business viability and scalability

Platform providers are the heart of a SCF ecosystem as they consolidate data produced through the ecosystem and share timely information to facilitate decision-making for supply chain activities and financing. It is therefore critical that platform providers ensure their businesses are sustainable and continue to drive scale, so promised value propositions to other actors and merchants are delivered. We have identified a few financial and non-financial levers platform providers can influence, in partnership to other actors, to drive growth and viability, including:

Increasing the percentage of active merchants. Actors can explore strategies such as increasing the basket of products which will encourage more merchants to use the platform, leveraging FMCG companies’ relationships to improve the quality of merchants during acquisition and extending the geographic reach of the platform.

Increasing the average order value. As merchants have access to market intelligence through the platform, they can understand and better predict demand cycles. Platform providers can leverage this and, combined with providing relevant and diversified products, can increase the average order value.

Increasing the percentage of loan requests. To achieve this, actors can explore a multi-FSP approach and increase the number of merchant-focused FSPs in the ecosystem. This will help provide more financing options and increase merchants’ access to finance or other related financial services.

Reducing the cost to acquire and serve merchants. There continues to be a heavy reliance on field agents by platform providers to acquire customers from the open market and use of same to drive customer engagement and support. Actors can collaborate and reduce onboarding costs by potentially increasing referrals from partner FMCG companies and distributors. As the platform technology matures and merchants become more comfortable with the platform, this can be used to drive and address basic customer interactions, leading to a leaner, more efficient agent structure and an overall reduction in operational expenses.

Improving terms with partners. Revenues for platform providers come from sharing fees and obtaining commissions from their partners. Platform providers will need to negotiate ideal rates with FSPs (revenue sharing from lending activities), FMCG companies/distributors (commissions on product sales), and logistics companies (logistic fees).

6. Have a clearly defined implementation strategy

While we acknowledge that actors are at varying levels of development, the implementation framework below provides a list of important activities that participants should consider when building a new model or scaling an existing one.

Planning

- Evaluate and select potential partners.

- Design model configuration and flow.

- Agree upon roles and responsibilities.

- Conduct legal processes and contractual agreements between partners.

- Assess implications of proposed ecosystem on existing business models.

- Assess resource and internal capacity requirements to drive implementation.

Preparation

- Define end state and major iterations to reach it.

- Gather requirements across actors.

- Develop platform to meet requirements (MVP or additional).

- Undertake integrations with FSP and develop credit scoring. Use existing data to test, where available.

- Undertake integrations with other actors: FMCG companies/distributors, logistic providers and payment providers.

- Prepare marketing awareness and engagement plan.

Engagement or Pilot

- Select existing merchants or onboard new merchants for the pilot.

- Perform limited test and pilot; work with limited distributors and geography.

- Incorporate learnings into the business processes and platform.

Expansion

- Continue to refine model to meet additional requirements.

- Onboard additional FSPs to expand financial product services.

- Onboard additional FMCGcompanies/distributors to expand product variety.

- Onboard other additional actors like logistic providers and payment providers.

Performance Monitoring

- Measure impact.

- Incorporate learnings into the business processes and platform.

Part 4: Optimizing MSME-focused supply chain finance in Africa

The lessons we have learned in Ghana, Ethiopia, and Nigeria are invaluable, as each of these countries represents varying levels of development of the ecosystem. The recommendations below therefore provide a good foundation and a blueprint for other actors across the continent looking to build new or optimize existing supply chain finance solutions, allowing them to further glean from the specifics around any of the three countries closely related to the nuances and individual issues they currently face. To ensure consistency, our recommendations have been structured around the building blocks stated earlier in this report.

Onboarding and integration into existing data sources: Building stronger partnerships with FMCG companies is key, as this can create more efficient options to onboard, handhold, and support merchants who will be interacting with the platform, many for the first time. This partnership allows platform providers to access and onboard quality merchants through referrals, provide wider product options, and mitigate against product unavailability or quality issues — key requirements from merchants. Partnerships may need to be elevated to the FMCG company level rather than with distributors or wholesalers, which is the current status quo and unfortunately usually transactional in nature. Moving from such transactional arrangements allows the FMCG company to be fully engaged in the SCF ecosystem and derive maximum benefits from it. FMCG companies can then onboard their key distributors who will work closely with the platform to fulfill and supply goods ordered through it and ensure integration is done between the platform and their existing sales fulfillment and other relevant operational systems. Furthermore, platform providers need to consider an omni-channel approach for onboarding. In doing so, they should assess the most efficient channels to onboard and provide handholding and change management to merchants, while effectively managing their costs and minimizing inefficiencies. This includes options such as on-the-ground agents (who could also serve as relationship managers), call centers, unstructured supplementary service data (USSD), and the use of social media channels that merchants are familiar with and can easily adapt to, such as WhatsApp.

Stock order management: Once onboarded, merchants should be encouraged to order via the platform so that transactions and data generated give a true representation of the merchant’s business. This is critical, as it allows the platform and other partners to utilize such information for credit scoring, analytics, and better decisionmaking. Additional provisions could be made to receive orders via a call center; however, this will be limited and only targeted at merchants who are interested but slow to adopt the digital channel. The order data can then be forwarded to key distributors of FMCGs or multi-FMCG distributors, who integrate their operational systems into the platform, for fulfillment. To ensure delivery times are maintained, the platform provider could explore delivery of stock directly to the merchant or extend their partnerships to third party logistics providers who can provide last-mile deliveries.

Relationship management: Ongoing relationship management is critical as this ensures the platform provider can receive feedback from merchants and promptly address issues relating to stock ordering and credit repayments. Riding on their omni-channel approach, platform providers need to have a good balance of self-service versus assisted-service, depending on the digital maturity of the merchants and the technology environment. As much as possible, platform providers should strive to develop and migrate merchants onto their digital channels and position assisted-service as an alternative option for merchants who are slow to adopt, using on-the-ground sales agents or call centers.

Payment services (conversion of cash to digital payments): Nudging and tactically moving merchants from cash to digital payments is important. The platform, working with FMCG companies and their distributors, needs to better leverage the growth in digital payments in their respective countries. This will require integrations of the platform and distributors into alternative but widely used digital payment infrastructures such as mobile money, bank-led wallets, and cash-in/cash-out agents. Partners could explore options, working with digital payment operators, to minimize impact of transaction fees so merchants are incentivized to start and continue with digital payments.

Credit management: Building strong partnerships with multiple FSPs is critical as this improves availability of funding and allows the platform provider to extend additional financial services. While there is a mixed approach of how supply chain finance is currently funded by platform providers, there has also been an increase in the number of FSPs that have embarked on their own digital lending journeys, developing and providing unsecured digital loans directly to merchants for their working capital needs. While this is a positive development, many FSPs would want to partner with platform providers who have demonstrated good loan portfolios within acceptable loss limits. It is incumbent on the platform to demonstrate this ability and showcase it as an effective credit management and monitoring process, supported by an effective relationship management approach. With the data available to it, the platform provider can then work with potential FSPs to utilize data analytics and algorithms to assess merchants’ creditworthiness and offer lending directly to the merchant for stock purchase. Integrations into these FSPs would be needed and the FSPs would need to adapt existing credit models, technology infrastructure, and processes to consume the data it receives from the platform. Upon successful disbursement, monitoring, repayments, and collections would be the joint responsibility of the FSP and the platform provider.

Liquidity for FSPs: For many FSPs, this may be a new journey as it deviates from their existing working capital products for MSMEs; for example, use of alternative data instead of the usual bank account transaction history as well as requests for collateral and guarantees. FSPs will need access to affordable funding to provide additional liquidity and manage the risk of unsecured lending to this segment. This funding could be a combination of low-interest loans, credit guarantee schemes, and grants provided by the government or development finance institutions (DFIs).

Value-added services: To improve adoption and usage, the platform provider will need to go beyond providing only lending and goods. It is important that they work with merchants in building their capacity to build their business and the resilience required to sustain it. While various solutions may be available, it is important that the platform provider properly assesses and identifies which solutions best resonate with the merchants it serves. From our research, value-added services such as loyalty schemes, capacity building, and insurance resonate strongly with many merchants. Based on this, the platform provider will need to form partnerships to validate, design, test, and evaluate the viability of those value-added solutions considered important by the target market. Partner FMCG companies can also extend their level of involvement by providing incentives directly to merchants, such as formalized discounts.

Ghana

Implementing a complex, multi-partnership ecosystem in Ghana would be challenging given that the SCF ecosystem is still in its development stage, with few platform-enabled players trying to prove their concept and gain traction. This provides an important opportunity to deepen the market and improve current offerings, but existing actors will need to be flexible and ready to modify certain elements of their business model to make the SCF ecosystem work effectively as envisaged.

While many platform providers have integrated their platforms to multiple digital payment infrastructures such as mobile money and cash-in/cash-out agents, the new 1.5 percent e-levy introduced in Ghana may require that partnerships with mobile network operators (MNOs) are key as they could provide a low-cost approach to digital transactions or provide various ways to incentivize merchants to start or continue with digital payment.

Ethiopia

Regulatory constraints and infrastructure underdevelopment has created a slow growth in the development of digital financial services. From a platform-enabled supply chain finance perspective, Ethiopia remains a greenfield with no SCF concepts in play. However, recent policy changes by the government, new initiatives such as the National ID, and the introduction of new players into several key sectors (e.g., Safaricom and M-PESA beginning operations in the country), as well as the increasing number of partnerships piloting digital solutions, provide an exciting opportunity to work with existing players to develop, pilot, and eventually scale MSME-centered SCF solutions.

The lack of actual SCF use-cases in Ethiopia means that many actors, specifically FSPs and FMCG companies, have no experience in fully implementing such platform-enabled solutions. A viable path could be to leverage nascent pilot programs — for example, digital unsecured lending pilots — and work with the proponents of these pilots to customize them for supply chain finance requirements. This ensures that the SCF framework takes advantage of several learnings from these pilots, shortens the time to market, and can meet the pain points of merchants.

These SCF solutions will need to find ways to address Ethiopia-specific constraints including a rudimentary National Identity scheme, sparse credit bureau data, and regulatory requirements that may inhibit fully digital loan contracts. For Ethiopia, recruiting and onboarding suppliers/manufacturers of locally made FMCGs and popular local other items such as spices is key for scale, as these form the bulk of the basket share for many MSMEs.

FSPs in Ethiopia will see this as a new and necessary journey, one taken with great caution, and it may require additional technical assistance and other support to update existing credit policies, processes, and operational systems to support SCF products. For example, FSPs will need to learn how to integrate sales order history and supplementary data on the merchant into their credit assessment models.

Nigeria

Supply chain finance in Nigeria is in the growth phase with several players in the market, ranging from larger platform providers, serving several thousand merchants, that have built workable models but require additional funding to provide credit to their growing merchants, to smaller platform providers that are looking to prove their concept and upgrade their business model and/or technology infrastructure.

This places Nigeria in a unique position, as some of the actors are familiar with platform-enabled supply chain finance models, with partnerships built with FMCG companies, their distributors, and independent multi-product distributors and wholesalers, but less so with FSPs. Though mobile money is not as well-developed in Nigeria as it is in Ghana, the emergence of payment service banks (PSBs) and MNO-led mobile money schemes is an opportunity to create partnerships with these entities to drive digitization of payments at scale, as well as leveraging ubiquitous agency banking operators as cash-in/cash-out agents.

The long-term viability of many of these models is still in question and systemic challenges including weak distribution infrastructure make serving MSMEs outside of major urban centers prohibitively expensive. Partnerships with logistics providers will be key to driving growth of platform-enabled SCF solutions.

Conclusion

Supply chain finance can be an effective tool to close the credit gap faced by small and micro merchants and to address other operational and market challenges.

Zewedu Addis is a small merchant in Addis Ababa who has been in the retail business for 13 years. Over the years, he has watched different business trends pass by. With the rapidly growing population in Ethiopia, Zewedu has noticed significant changes in the preferences of the end consumers. He has discovered that there is high demand for products generally, but merchants cannot meet their customers’ demands due to inadequate working capital. He says, “If you can buy, you can sell because the demand is always there, but to buy, you need cash.”

Zewedu sees several potentials in a SCF product and will use such a financial tool to tap into the opportunities in the rising demand for FMCG products in Ethiopia. A SCF product will help last-mile merchants like him expand their businesses and invariably increase their revenue. It will give them the flexibility to buy different products and offer the end consumers more variety, which will allow them to cope with economic shocks and be more resilient.

The above story of Zewedu summarizes the essence of this report. Supply chain finance has the potential of helping last-mile merchants, targeting merchants who are looking to stabilize or grow their business. These merchants value the timely access to credit and inputs that SCF can provide, and the business advice and additional services that can be tailored to them based on the data generated.

Supply chain finance can be an effective tool to close the credit gap faced by small and micro merchants and to address other operational and market challenges. When done right, SCF can provide the millions of small merchants in the chain financial security and reduce the percentage of the working poor in Africa, leading to a more sustainable livelihood for the rapidly growing population of women and youth on the continent.

This paper is supported by the Mastercard Center for Inclusive Growth.

Contributions from Simon Aderinlola (Nigeria), Kwashie Agbitor, Iain Brougham, Melssaw Gessesse (Ethiopia), and Ophelia Ama Oni (Ghana).

Cover photo: Maa Afia, a micro retailer in Accra, Ghana