This publication is based on research funded by the Gates Foundation. The findings and conclusions contained within are those of the authors and do not necessarily reflect the positions or policies of the Gates Foundation.

We would like to thank the foundation for its support and all the partners named in this report for working with us on this project.

Executive summary

Smallholder farmers are the backbone of global food production. In most low and middle-income economies, they are the largest food producers, and agriculture is often the most significant employment sector. Their role is crucial, and their challenges must be addressed to ensure food security. Despite limited access to credit, markets, and advisory services, compounded by climate-related issues, smallholder farmers continue to demonstrate resilience and determination.

Access to fit-for-purpose, affordable, and sustainable finance is a key enabler to improve productivity for smallholder farmers. Unfortunately, roughly 70 percent of the global credit demand for smallholder farmers, upwards of $170 billion USD, remains unmet annually. This gap can be attributed to several key factors:

- Financial institutions often consider smallholder farmers too risky to lend to.

- The absence of specialized financial products poses a significant barrier to accessing the essential financial tools required in the agricultural sector.

- Smallholder farmers often do not have access to physical bank branches nearby to inquire about or apply for financial products and services.

- Smallholder farmers often lack collateral and cannot access crucial financial support, which hinders their ability to invest in their farms and livelihoods.

The absence of formal financial backing often drives smallholder farmers to seek alternative funding sources and rely instead on informal lending, stressing the need for tailored financial solutions. The challenges mentioned above are worsened by the effects of climate change, which amplify the difficulties related to smallholder farmers’ productivity, health, and livelihoods. Increasing smallholder farmers’ resilience to climate change and decarbonizing the agriculture value chain in developing countries is crucial. A key step to achieving these goals is to provide smallholder farmers with the necessary tools, information, and access to credit while ensuring any products developed and changes in distribution are relevant to them.

Financing enables smallholder farmers to make investments that enhance their climate resilience, productivity, and livelihoods. Additionally, financing at the intersection of climate and agriculture presents a unique opportunity to transition from a dominant fossil fuel-based value chain to a green one by providing access to finance for greener initiatives and assets. With that in mind, Accion led efforts to demonstrate innovative asset financing models for smallholder dairy farmers in India and Kenya. With a focus on serving women, these models included milk receipt-based financing, product bundling, and program financing approaches specifically.

As we explore our findings in this report, it is important to recognize that piloting innovative asset financing models requires time and can face unforeseen challenges, despite strong stakeholder commitment. These complexities underscore the importance of philanthropic funding to support experimentation, absorb risks, and pave the way for scalable solutions with long-term impact.

With support from the Gates Foundation, Accion developed a program to establish partnerships within the dairy farming ecosystem to test various asset financing demonstration models and identify potential ways to scale them.

Accion acted as a catalyst to achieve the project scope and collaborated with many ecosystem players in both markets, including financial service providers, dairy service providers, agritech companies, and original equipment manufacturers (OEMs). We explored and gained constructive insights in three key areas: partnerships, product, and gender.

Introduction

Smallholder farmers in India and Kenya, particularly women, are less likely to have access to affordable financial services, especially for productive assets such as water tanks and biodigesters.

Agriculture is the backbone of the economy in India and Kenya, accounting for a significant portion of each country’s Gross Domestic Product (GDP). The dairy sector alone contributes five percent to India’s GDP and between three and four percent to Kenya’s GDP. Smallholder dairy farmers in both countries, particularly women, are less likely to have access to affordable financial services, especially financing for productive foundational and complex assets such as water tanks and biodigesters.

Moreover, the productivity gap compared to global north economies is staggering. The average daily milk yield per cow in India and Kenya is roughly four liters, compared to 14 liters in the Netherlands. Access to finance not only enables smallholders to invest in productive assets, but also afford nutritionally dense forage, proactive veterinary care, and better infrastructure to manage water supply.

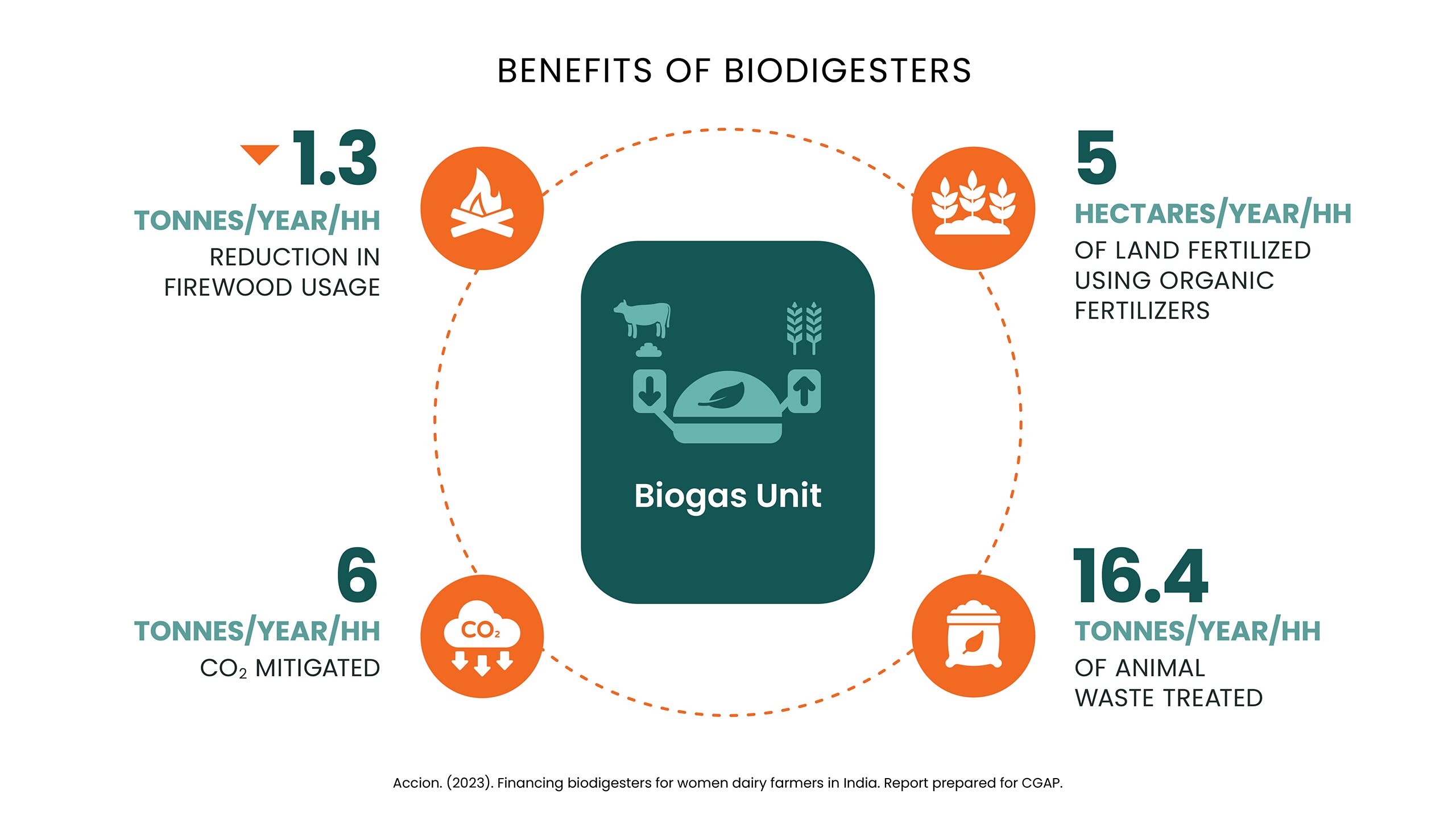

Through initial research in India and Kenya, Accion identified several key barriers to higher adoption of productive assets such as biodigesters. Biodigesters are systems that convert organic waste to methane fuel and other useful by-products. They have the potential to significantly improve the socio-economic, environmental, and health outcomes for smallholder farmers and their households. However, biodigester adoption in India and Kenya has been much lower than expected.

Barriers to adopting biodigesters:

- Affordability: Many smallholder farmers are deterred by the relatively high upfront costs to purchase and install biodigesters. The initial cash outlay often presents a trade-off between short-term needs, such as household requirements and production needs, versus long-term cost savings.

- Access: Smallholder farmers lack access to affordable credit and funding mechanisms. Women smallholder farmers encounter even more significant hurdles as they often face social, economic, and normative constraints that systematically inhibit their access, usage, and control over finances and productive resources.

- Perceived financial risk: Financial service providers and other lenders are reluctant to offer credit to smallholder farmers because they perceive them as high-risk and expensive to serve.

- Knowledge gap: While biodigesters provide several health, agricultural productivity, climate, and economic benefits, smallholder farmers’ ability to fully realize these benefits is constrained by persistent misconceptions, misinformation, and a general lack of awareness. Farmers are unfamiliar with maximizing gas and bio-slurry output to make productivity gains, substituting methane gas to save costs, and the potential for higher crop yields and revenues from selling bioslurry or selling organic crops that use bio-slurry instead of chemical fertilizers at higher prices.

- Limited ecosystem engagement: The knowledge gap is exacerbated by limited support from the broader ecosystem in the dairy value chain. There is an opportunity to deepen engagement, increase knowledge sharing, and enable better biodigester usage practices.

The project: Exploring asset financing demonstration models in India and Kenya

These barriers informed our work on this project, which aims to demonstrate pathways to viable, sustainable impact financing for smallholder farmers and enable them to purchase productive assets — in this case, biodigesters in India and water tanks and chaffcutters in Kenya.

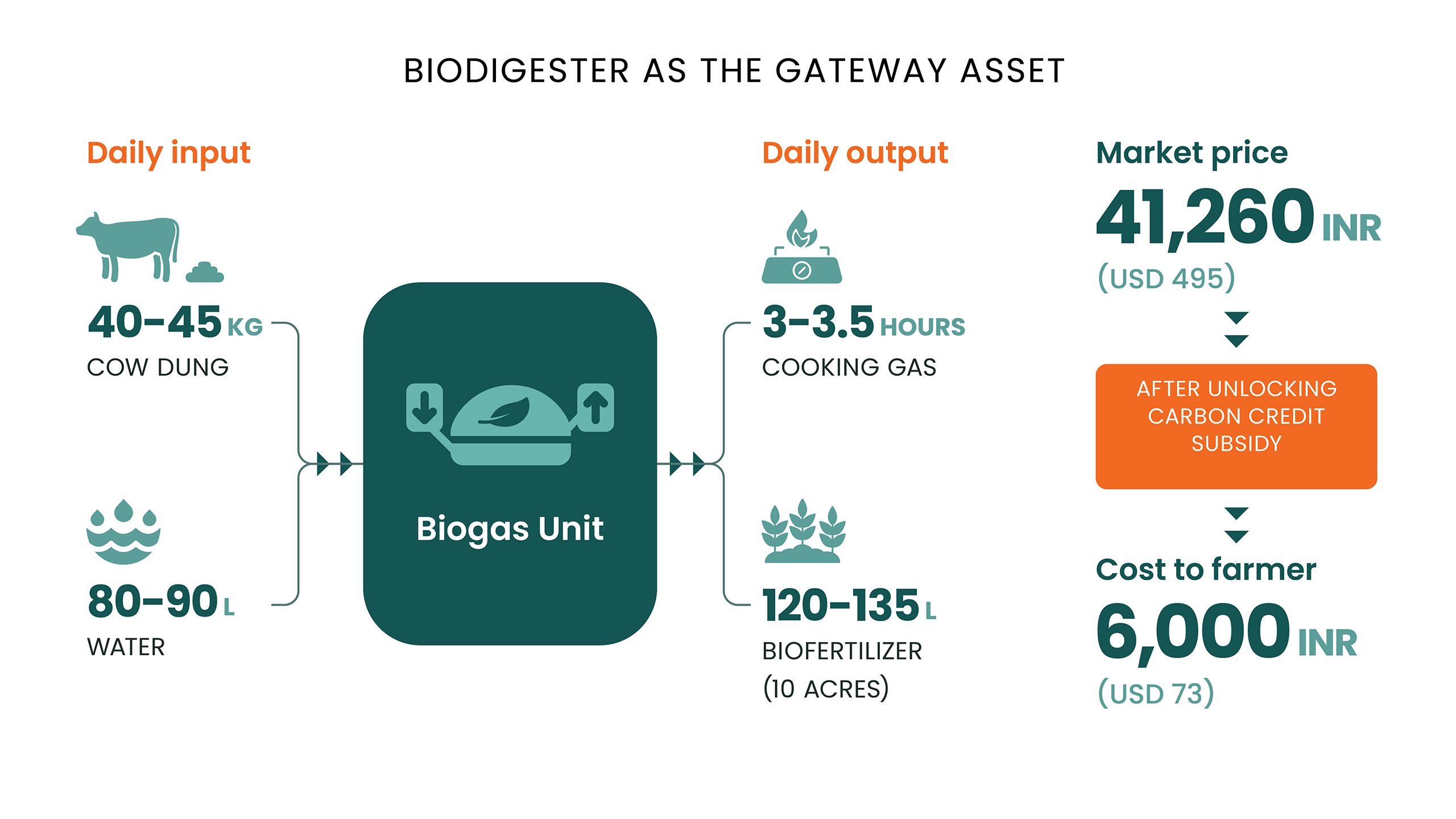

In India, Accion selected biodigesters as the gateway asset for this project because they represent an asset category that is atypical for most lenders, which is important for a few reasons. First, by targeting an unconventional asset, the project aims to unlock financing options for smallholder farmers who have traditionally been overlooked by lenders. This focus on biodigesters allows for the introduction of innovative financing solutions tailored specifically to the needs of farmers, recognizing the significant role these assets play in enhancing agricultural productivity and cost reduction of cooking fuel. Also, addressing the financing gap for biodigesters not only supports sustainable agricultural practices but also promotes energy efficiency and environmental sustainability. Biodigesters demand more customer support for installation and operations and comprise a significant portion of the farmer’s income. This requires a more complex financing product than the standard productive assets lenders are comfortable financing for smallholder farmers. Except for OEMs and a few other entities (primarily via government or donor subsidies), few lenders or credit products cater to these types of assets.

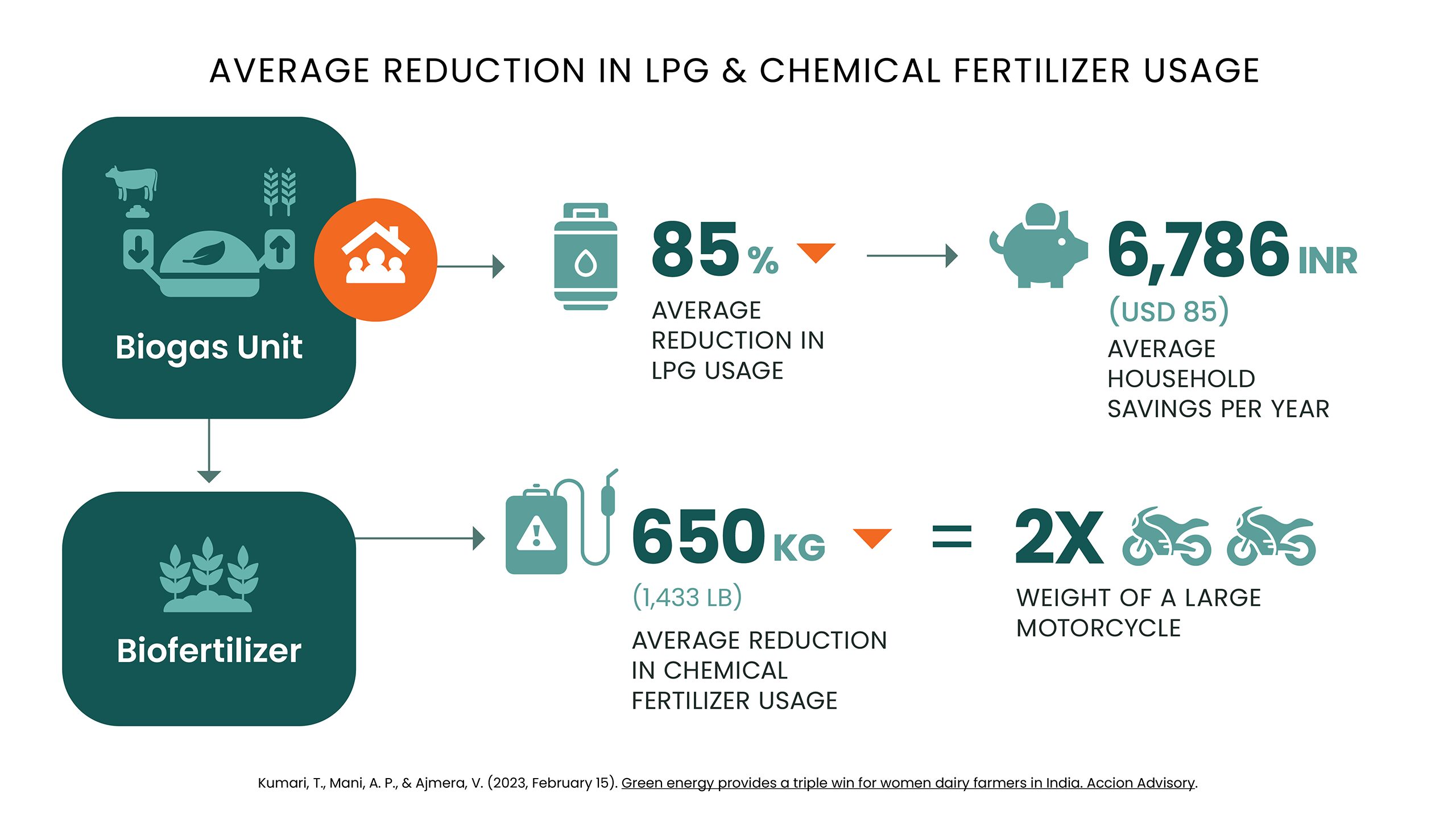

For instance, a smallholder farmer with three to four cows investing in a biodigester can significantly benefit from an average 85 percent reduction in LPG usage, translating to annual savings of approximately ₹6,786 ($85 USD). This investment not only alleviates household expenses but also reduces the reliance on chemical fertilizers by around 650 kg (1,433 lb), about twice the weight of a large motorcycle — every year, promoting sustainable farming practices.

Also, smallholder farmers carefully assess complex assets like biodigesters by weighing long-term economic benefits, installation complexities, and ongoing maintenance costs. Their decision-making process involves understanding how the biodigester will impact daily farming operations, whether it fits within their capacity to manage new technology, and whether the potential returns from both productivity gains and new income streams (e.g., bio-slurry sales) justify the initial investment. The biodigester fits this bill as it comes with tailored support for installation and operation, ensuring ease of use for farmers while helping to reduce costs and creating additional income opportunities.

Secondly, biodigesters also make a good case study for understanding how ‘complex’ assets can significantly deliver economic benefits to smallholder farmers because of the potential not only for productivity gains but also for new income generation (e.g., bio-slurry sales).

From financial service providers’ perspective, offering financing solutions for productive assets such as biodigesters is an opportunity to evolve and enhance their customer appraisal processes by incorporating parameters like cost savings or income increases when calculating a customer’s income flow. For instance, if a customer is using two LPG cylinders per month that each cost approximately ₹1,000 ($12.5 USD), switching to a biodigester could translate to monthly cost savings of ₹2,000 ($25 USD). This amount can be factored into the appraisal as an equivalent income increase, reflecting the economic value the investment brings to the household.

However, while such information provides a clearer picture of a customer’s financial capacity, they serve as proxies and require validation to ensure they accurately represent the utility on the ground. This often demands robust technologies or processes, which can be time-consuming and expensive and ultimately increase the cost of credit for the customer. To address this challenge, investments and innovations in technologies that support monitoring, reporting, and evaluation are critical for ensuring accurate appraisals without disproportionately burdening the customer. These factors underlie the complexity of and need for developing suitable financing options.

In Kenya, many smallholder farmers resort to old-fashioned tools to manage their operations due to a lack of access to advanced farm equipment and machinery. Our survey with farmers in the Central and Rift Valley regions indicated a need for labor saving solutions such as water tanks and chaff cutters, hence the program’s focus on these assets for financing. With nearly 67 percent of Kenyan households lacking piped water, access to water is critical for both home and farm operations. Water tanks are helpful adaptation tools necessary to combat climate change-induced irregular rainfall patterns and their impact on agricultural productivity and overall chores for women. Chaff cutters are time and effortsaving equipment necessary for feed harvesting and processing, helping to break down fodder materials such as maize stalks into smaller digestible pieces. Farmers using chaff cutters reported improvements in farm efficiency, animal health, milk production, and income.

We explored innovative funding mechanisms and related activities that quantify and maximize benefits from these assets for the entire household. The demonstration models created will inform service providers’ asset financing product design and help scale the number of farmers served and the types of products financed.

We measured project outcomes by capturing sex-disaggregated data through impact assessments. These assessments measure biodigester usage and the resulting gain in household savings, income, and productivity. They also measure the impact of reducing women’s drudgery and enhancing their access to and agency over their income from dairy farming.

We recognized the importance of capturing data specific to women given the critical role they play in adopting and using assets like biodigesters, particularly in rural areas where they manage household energy and waste systems. As primary caretakers, women benefit directly from the clean cooking fuel biodigesters provide, reducing reliance on firewood and mitigating health risks from indoor air pollution. Women often handle daily operations, including feeding organic waste into the biodigester. Their involvement ensures not only that the biodigester operates effectively but also that their household can realize broader benefits such as improved health, income, and sustainability.

Our approach

Accion’s extensive experience in inclusive finance and our ecosystem approach was instrumental in meeting the project’s objectives and informing its design and delivery. We collaborated with financial service providers, dairy service providers, agritech enterprises, and OEMs. We also leveraged our product development expertise to design tailored solutions that address the unique needs of smallholder dairy farmers.

From the outset, we took a gender-smart approach to product design. We considered women’s awareness of, access to, and agency over productive resources to design gender-responsive product bundles and customized service offerings that meet women farmers’ financial priorities and lifecycle needs.

By addressing the intersecting challenges of financial inclusion, women’s economic empowerment, and climate resilience, this initiative not only supports the livelihoods of smallholder dairy farmers but also contributes to broader goals of sustainable development and poverty alleviation.

It is also important to highlight that market-level nuances informed the approach in India and Kenya. The program was designed to demonstrate productive asset financing models that enable reach and access for smallholder dairy smallholder farmers, especially women in both markets. The catalytic funding from the Gates Foundation was leveraged to stitch together ecosystem partnerships in the existing regulatory structures to identify and develop commercially viable partnership models that have the potential to scale. Notably, given the 15-month program duration, Accion prioritized interventions and partnerships that offered the best opportunity to test and learn for viability. Therefore, the insights shared in this report were gathered while navigating the broader market condition and the enabling environment.

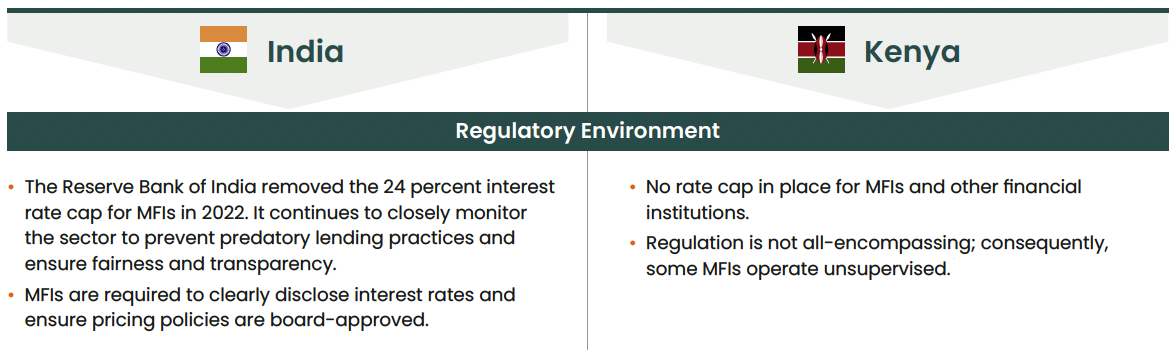

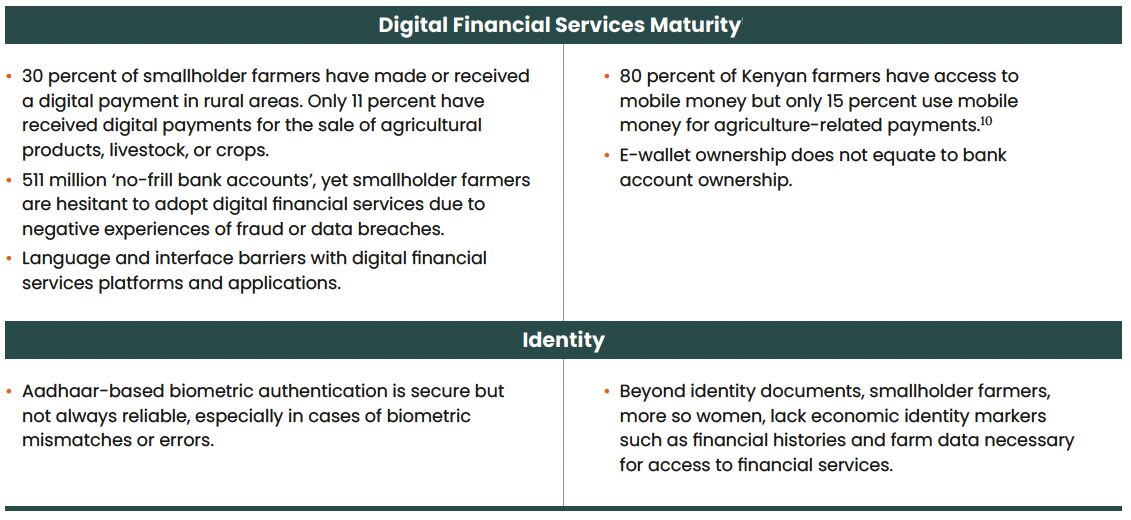

Below are some key differences that impacted the approach across the two markets:

When effectively designed and deployed, innovative financing models, supported by the right regulatory support, can significantly democratize access to credit for marginalized and underserved populations, especially smallholder farmers.

Insights

The dairy sector presents unique ecosystem challenges that underscore the need for robust partnerships to enhance reach, financial accessibility, and farmer productivity.

Partnerships

Partnerships play a crucial role in addressing the challenges faced by smallholder dairy farmers in India and Kenya. The dairy sector presents unique ecosystem challenges, such as fragmented financial markets, high transaction costs, and limited access to credit. These challenges underscore the need for robust partnerships to enhance reach and financial accessibility and ultimately improve farmer productivity.

Partnerships are pivotal in bridging gaps within the dairy value chain, particularly asset financing. Bringing together various stakeholders, including financial service providers, OEMs, and agritech, can offer comprehensive solutions that address both financial and operational challenges. Integrating innovative models and collaborative efforts ensures that smallholder farmers can access the resources and support they need to thrive.

Accion deliberately identified partners across the value chain to test and learn how differing partnership models are positioned to scale. More importantly, the partnership structures were conceived to unlock financing flow to smallholder farmers in both markets. In the product section of the report, we detail the underlying products designed through the partnerships.

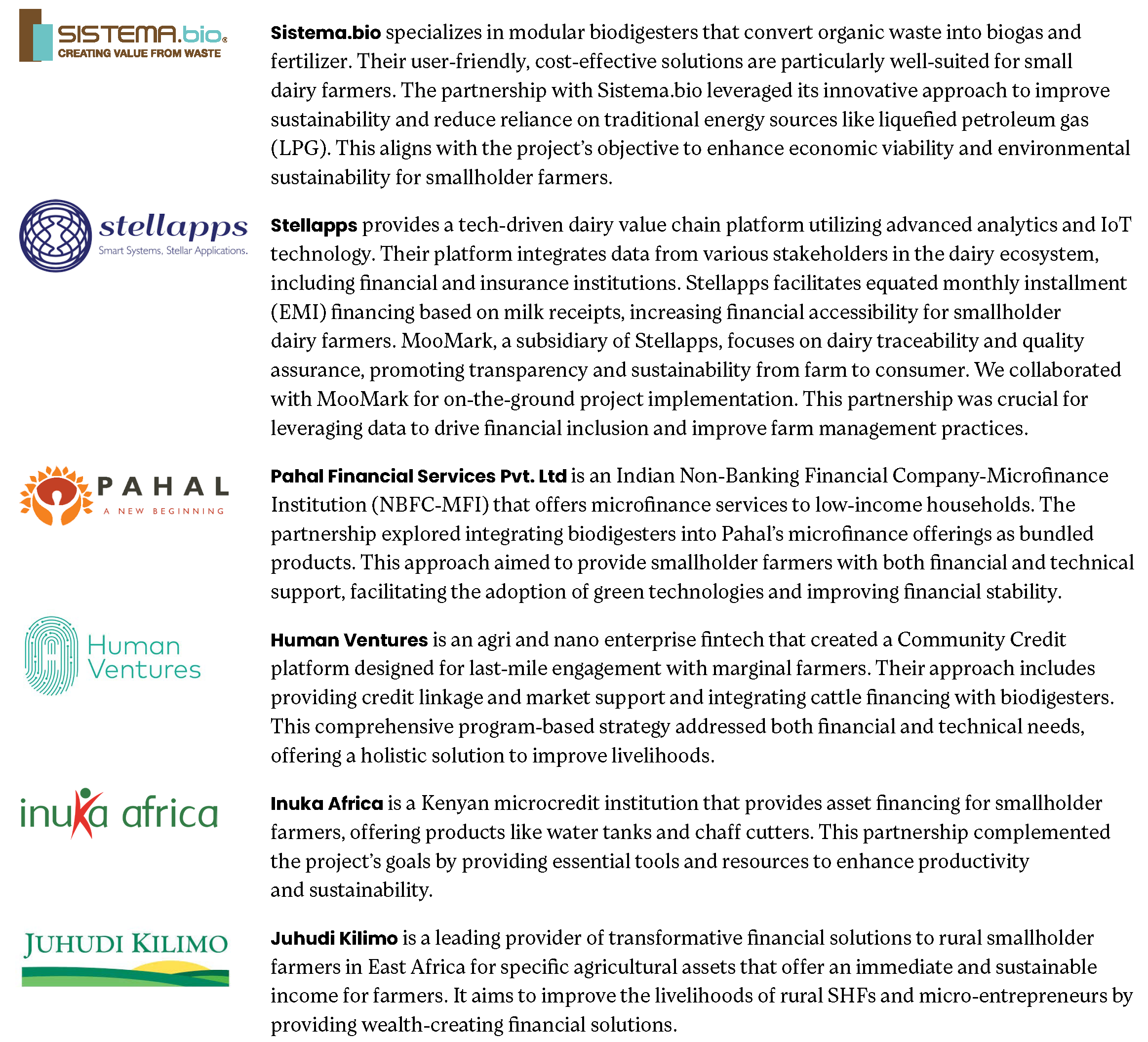

Key partners and their roles

The project leveraged tailored partnerships in India and Kenya to deliver asset financing solutions that align with each country’s specific agricultural ecosystem and farmer needs. In India, partnerships emphasized technology-driven solutions and bundled financing models to integrate biodigesters into farmers’ daily operations, leveraging data for improved financial access. In Kenya, the focus was on creating access to essential productivity tools and market linkages through partnerships that support dairy farming with a holistic approach. Each partner brought unique expertise, from asset financing to techdriven solutions, creating an ecosystem tailored to smallholder needs in each region.

In both markets, these targeted partnerships brought together finance, technology, and resources tailored to local smallholder needs, creating an ecosystem that supported adoption and sustainable practices unique to each region. Details of each partner are mentioned below.

Lessons learned

Partnerships geared to serve the smallholder farmers at the last mile must address critical gaps associated with access to finance and awareness creation for any meaningful opportunity to drive traction and scale. Mainly where partnerships are intentional about scaling innovative products and services, affordability to smallholder farmers is a vital enabler for scale.

Therefore, aligning expectations and requirements across partners and from boardrooms to branches is vital for executions. Through the project, we identified and engaged over 20 partners across the two markets and onboarded nine partners.

The complexities of facilitating a collaborative ecosystem and navigating market dynamics in two countries generated several key learnings:

1. The significance of a ‘catalyst’

The role of a catalyst is essential in stitching together the ecosystem. The product manufacturer would not typically take on this role because it would require capabilities that are not core to its business. Product manufacturers have partnership teams that focus on increasing traditional distribution channels. However, many are not well equipped to identify non-traditional partners such as platform, data, and financial service providers, or to structure inclusive customer acquisition that considers the appropriate financing mechanisms and capacity-building requirements for the end customer. Ideally, the catalyst would have the ability to bring a funding partner to the table to experiment and pilot various business models.

Effective partnerships require a strategic approach to identify and connect various stakeholders, each bringing unique strengths to the table. Particularly, the role of a catalyst is vital in staying with the problem and also taking a neutral position in mediating concerns. For instance, initially, we focused on creating micro process flows to map out every detail and ensure clear guidelines for all parties. However, we quickly realized that this alone was insufficient. To make more informed and impactful decisions, we conducted field visits, engaging directly with partners and observing on-the-ground realities. These visits provided critical insights, allowing us to adjust strategies based on firsthand observations and tailor solutions to meet each partner’s specific needs. Also, we intervened in the commercial processes to balance the interests of all parties, ensuring that the solutions were feasible and aligned with each partner’s operational requirements. By actively facilitating these processes and staying connected with partners, we could drive collaborative progress and foster a more cohesive ecosystem that encouraged sustainable growth and scalability for all involved.

2. Commercial viability

Structuring partnerships around commercial viability increases the likelihood of long-term sustainability. By focusing on designing products that were both affordable for clients and commercially viable for partners, the project aligned interests, securing commitment from all parties and enhancing scalability beyond the project duration. A key example of this approach was the development of a bundled product for one of the partners. This product included both the asset and additional services, allowing the partner to absorb servicing costs while still maintaining affordability for the end client. This bundling strategy ensured that the solution could remain financially feasible and operationally sustainable even after the project’s end. By prioritizing accessible financing and well-aligned pricing structures, the project helped foster a commercially sound model that could be scaled effectively, benefiting both partners and clients in the long term.

3. Building trust is complex and time-intensive

Strengthening collaboration across diverse players involves identifying and understanding trust levers. Establishing clear communication, shared goals, and mutual benefits is crucial for fostering successful partnerships. Mission alignment among stakeholders laid the groundwork for a collaborative environment where partners felt encouraged to experiment with different business models. However, establishing this trust required careful attention to each partner’s unique needs and substantial investments in resources, time, and operational support. A key element of this trust-building approach was actively seeking opportunities to support partners beyond their immediate needs or requests. By proactively offering assistance in go-to-market (GTM) activities and capacity-building initiatives, the project team demonstrated commitment to partners’ success. This included understanding their specific challenges, providing resources, and dedicating time to resolve issues—even when the support was not formally requested. This willingness to invest in their development fostered stronger connections and trust, showing partners that the project team was genuinely invested in their growth.

4. Reaching the tipping point

Reaching a tipping point was crucial for driving adoption and deepening last-mile product offerings among smallholder farmers. Achieving this critical mass enabled the project to scale solutions effectively and secure sustained uptake. In this 15-month project, significant traction was observed in the final three months, underscoring the need for sufficient time for gradual adoption and understanding of green assets. This outcome highlighted a key insight for agriculture-focused initiatives: extended project timelines are essential to allow partnerships to mature and support multiple crop cycles. These cycles are critical for testing, refining, and proving solution viability. With additional time, partners can iteratively adjust product offerings across diverse seasonal conditions, collect comprehensive feedback, and make more informed decisions on scaling strategies. Longer timelines also support an in-depth analysis of agricultural cycles, allowing partners to pinpoint the most effective methods for achieving lasting impact among smallholder farmers.

5. Unintended consequences

By integrating innovative solutions and leveraging the strengths of various stakeholders, these collaborations are paving the way for improved financial access and enhanced productivity in the dairy sector.

The diversity of stakeholders led to several unintended yet beneficial outcomes, including the crowding in of similar actors that opened opportunities for new collaborations beyond the project’s initial scope. While this can create a broader impact, it also highlights the need for strategic partner selection and management to avoid redundancy and maximize impact. For instance, dairy intelligence platform Dvara E-dairy explored partnerships with Pahal and Inuka, while global climate insurtech IBISA engaged in discussions on parametric insurance solutions with Pahal. Although we were unable to formalize these partnerships due to the project duration, they created a synergistic environment where likeminded organizations could share resources and expertise, reinforcing the ecosystem and allowing innovative product expansions tailored for smallholder needs. This synergy demonstrates the potential for strategic collaboration beyond project timelines, expanding the reach and impact of each partner’s efforts.

The types of partnerships formed under this project are instrumental in addressing the multifaceted challenges faced by smallholder dairy farmers. By integrating innovative solutions and leveraging the strengths of various stakeholders, these collaborations are paving the way for improved financial access and enhanced productivity in the dairy sector. The lessons learned from these partnerships emphasize the importance of strategic alignment, trust-building, and thorough planning in creating sustainable solutions for smallholder farmers in India and Kenya.

Product

Smallholder farmers in India and Kenya, particularly women, have limited access to affordable financial services that can help them acquire productive assets such as biodigesters, chaff cutters, solar panels, and water pumps, which can drive productivity gains.

To maximize asset financing learnings from this project, Accion explored opportunities and supported the product development process with various partners (as detailed in the section above) to include or bundle financing for related productive assets in the dairy value chain appropriate for smallholder farmers, particularly women.

In India, we leveraged the carbon finance market to unlock a subsidy for the biodigester asset, which qualifies for carbon credits by reducing methane emissions through converting organic waste into biogas, a cleaner energy source. Additionally, the use of biodigesters reduces the need for LPG and firewood, further lowering carbon emissions. The market price of a biodigester is 41,260 INR ($495 USD), but after applying the carbon credit subsidy, the cost to the farmer is reduced to 6,000 INR ($73 USD). This approach made the assets more affordable and helped support sustainable farming practices.

Product types pursued

Milk receipt-based model (Sistema-Stellapps)

The milk receipt-based model developed between Stellapps and Sistema.bio uses data from smallholder farmers’ milk sales to facilitate financing for biodigesters. Stellapps was ideally suited to implement this model due to its advanced tech-driven platform that collects and processes milk data from various dairy stakeholders. By leveraging Stellapps’ IoT and data analytics capabilities, the partnership ensured that milk receipt data could be used to create accurate, timely, and risk-mitigated credit assessments, making it feasible for smallholders to access financing based on their regular milk sales.

Accion played a key role in developing this model by leveraging its expertise in financial inclusion and product design. Through analyzing milk receipt transaction data, Accion helped create a financing structure that aligns with farmers’ cash flows, enabling manageable EMI payments and encouraging adoption of biodigesters. This design approach ensured that the financing model was practical and fit the income cycles of smallholder farmers.

To promote adoption, Accion also supported community engagement by organizing street plays to raise awareness among local communities and incorporating gender-intentional collateral practices, ensuring that the financing model was inclusive and accessible for women smallholders. This multi-faceted approach helped Accion, Stellapps, and Sistema.bio bridge the gap between innovative finance and community-based engagement.

Product bundling (Sistema-Pahal)

Product bundling involves offering biodigesters as part of a cattle loan package. This model combines financial support for purchasing cattle with the provision of biodigesters, creating a comprehensive solution for smallholder farmers. Bundling these products helps address farmers’ immediate financial needs and long-term sustainability goals. Biodigesters offer benefits such as reduced reliance on LPG for cooking and improved waste management, contributing to both economic and environmental sustainability.

Pahal’s commitment to environmental, social, and governance (ESG) principles was instrumental in promoting biodigesters as a productive green asset among their rural customers. Recognizing smallholder dairy farmers as a critical demographic, Pahal identified biodigesters as a valuable solution for utilizing cow dung — a readily available raw material — to produce biogas. This innovation provided an alternative to LPG, often inaccessible in rural areas, and produced bio-slurry, an organic fertilizer that enhances agricultural sustainability.

In collaboration with Accion, Pahal developed targeted financial products to make biodigesters more accessible. The “Top-up Asset Loan” allowed existing cattle loan customers to purchase biodigesters with additional funding for dairy infrastructure improvements. A flexible installment plan was also introduced, enabling new and existing customers to acquire biodigesters through manageable payments. These financial solutions were tailored to meet the needs of rural farmers, ensuring they could invest in this green technology without significant financial strain.

However, we identified gaps while executing these strategies. For example, we needed to refine the incentive structures for adopting biodigesters to enhance their effectiveness. Training focused on the technical aspects of biodigesters, effective communication strategies, and gender-sensitive marketing approaches was provided, but a more detailed breakdown of incentives was necessary to ensure optimal uptake and impact at the grassroots level.

To ensure effective promotion and uptake, Pahal and Accion provided comprehensive staff training and developed marketing collateral appealing to both men and women. Demonstration units were placed near branch locations, and outreach activities such as street plays and organized farmer visits to demo sites helped build community awareness and trust. Despite these efforts, it became clear that further adjustments to the incentive structures and ongoing community engagement were essential for maximizing the impact of biodigesters. Still, 50 biodigesters were adopted in districts like Kheralu, Borsad, and Palanpur, demonstrating both the potential and the need for continuous refinement in approach.

Program financing (Sistema-Human Ventures)

Program financing for farmer groups focuses on de-risking clusters of smallholder farmers by providing technical assistance, financial support, and market linkages. This model integrates cattle and biodigester financing with technical support for implementing biodigesters, creating a cohesive program that addresses multiple aspects of dairy farming. By offering technical assistance and market linkages, this approach helps smallholder farmers adopt and effectively use new technologies, reducing risk and enhancing overall productivity.

However, a cluster-based financing model like this requires the financial service provider partner to share collective risk. Also, several key elements, such as identifying the geographical cluster, forming a group of dairy farmers, and conducting outreach, need to align for success. While we set up a demo unit for farmers, it could not be offered to the cluster without an aligned partnership. Due to the complexity of aligning all these elements within the project timeline, the partnership did not proceed as planned.

Asset financing model (Inuka Africa)

The asset financing model provides loans specifically for purchasing essential tools such as water tanks and chaff cutters. These tools are critical for improving dairy farm operations and productivity. By offering targeted financing for these assets, the model supports smallholder farmers in acquiring the necessary equipment to optimize their farming practices while serving as collateral for the financier. Along with Inuka Africa, we engaged 177 farmers — 57 percent women — in Nakuru and Nyandarua Counties over a four week period. Of these leads, only three farmers — two women and a man — received financing. The low traction was largely due to competition stemming from rural savings and credit cooperative societies (SACCOs), which provided more affordable financing compared to our partner MFI’s offering — credit-only microfinance institutions usually have a higher cost of capital because they lack access to cheap deposits/capital. This, combined with the high cost of serving rural communities, translates to more expensive loans compared to the SACCOs. Additionally, the farmers we engaged were part of community groups, and they were more interested in obtaining group loans, a model that Inuka Africa did not operate, resulting in the rejection of nearly 60 applications alone. Other requirements, such as the need for two to three guarantors, a cash deposit, and/or collateral — a model not unique to our partner MFI — created a barrier for the smallholder farmers. With the number of farmers who ultimately received asset finance loans not matching the resources invested in lead generation, all partners involved decided to call off the exercise. Nevertheless, our attempt generated numerous insights and learnings, which we outline in the subsequent section.

For further exploration

Pursuing these four distinct product types and managing each partnership presented valuable lessons and opportunities.

1. Customized lending options for fluctuating incomes

Seasonal variations in dairy production significantly impact the income of smallholder farmers. Higher yields during peak seasons and lower production during off-peak periods create fluctuations in income, making it essential to offer customized lending options. Flexible lending products that accommodate these income variations are crucial for supporting smallholder farmers. Collaborating with lenders who understand the unique financial needs of dairy farmers ensures that the products offered align with their seasonal income patterns.

2. Addressing customer challenges and perceptions

Understanding and addressing the challenges faced by smallholder dairy farmers is vital for the success of any product offering. Engaging actively with the dairy farming community through product demonstrations and feedback sessions helps in identifying and resolving any negative perceptions or obstacles. Promptly addressing issues related to installation or operation enhances user experience and facilitates the adoption of new products.

The product models designed and developed through this project address both financial and operational challenges faced by smallholder farmers in India and Kenya. Our experience highlights the importance of customizing lending options to accommodate income fluctuations and actively engaging with customers to address challenges and perceptions. These insights are critical for refining product offerings and ensuring their effectiveness in supporting the dairy farming community.

Gender

Using biodigesters in dairy farming presents an opportunity to enhance productivity and sustainability. However, gender dynamics and social norms significantly influence successful adoption. Women dairy farmers, often marginalized and facing unique challenges, require targeted interventions to fully benefit from biodigester technology.

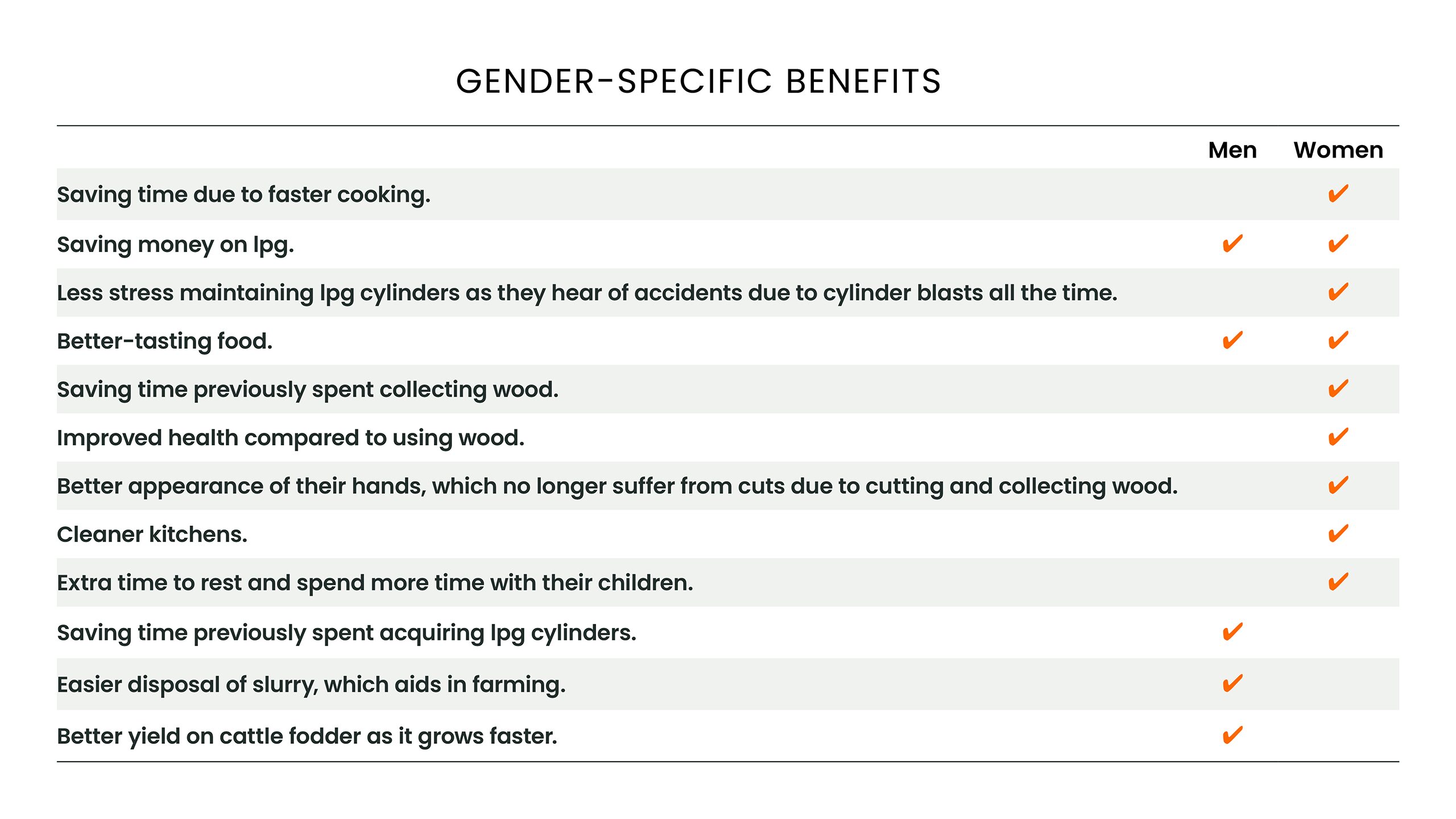

This project aimed to impact women dairy farmers by empowering them with greater independence and improved health and decision-making ability. Asset financing for women in the dairy sector can boost economic inclusion and enable women to take control of their livelihoods. By facilitating access to essential assets like biodigesters, we can help women dairy farmers significantly improve their productivity, reduce their workload, save energy costs, improve sanitation, and create an opportunity to increase their income. Biodigesters convert animal waste into biogas and organic fertilizer, addressing waste management issues and providing a renewable energy source.

For women dairy farmers to access asset financing, they must first interact with financial service providers’ field staff, who facilitate the application and approval process on behalf of the institution. However, there are inherent challenges within this relationship dynamic to overcome to increase women’s biodigester adoption rates.

Challenges faced by field staff

Financial service providers’ field staff are key to women dairy farmers’ access to biodigesters and other productive assets as the main point of contact with the institution. However, field staff often exhibit convenience-based gender bias in their approach to customers, predominantly targeting male farmers who they assume are the primary decision-makers. This bias stems from a combination of cultural norms and practical ease, as field officers, mainly men, feel more comfortable interacting with their male counterparts. This discomfort limits their outreach to and support for female farmers, who play a crucial role in dairy farming but are frequently overlooked.

Male field officers also often lack training in gender-intentional communication, hindering effective engagement. Additionally, field staff may lack the necessary skills and knowledge to address the unique needs and concerns of female farmers, leading to a one-size-fits-all approach that fails to consider gender-specific dynamics.

Challenges faced by women customers

Women dairy farmers encounter multiple obstacles in accessing and using biodigesters. Cultural and societal norms influence their involvement in farming activities, access to resources, and decision-making power. Decisions regarding asset acquisition and usage are predominantly made by male family members, hindering women’s ability to independently secure and utilize financial resources. This lack of agency in decision-making and reliance on the family patriarchs to make purchase decisions slows down women’s adoption process. Despite the benefits, women also perceive servicing biodigesters as an extra burden on top of an already significant workload, further discouraging adoption.

Client Spotlight

Curating inclusive and empowering marketing communication for women dairy farmers

Effective communication is key to encouraging women farmers to adopt biodigesters. Marketing materials should use inclusive, empowering, and relatable language and imagery that reflect the roles and aspirations of women in dairy farming. Feedback from women farmers themselves can help develop marketing materials that speak directly to their experiences and aspirations. Sharing success stories of women who have adopted biodigesters showcases the tangible positive impact on their lives, emphasizing transformations in income generation, household tasks, and overall well-being. Disseminating these success stories through various channels, including community meetings, social media, and local media outlets, can inspire and motivate other women farmers.

Usha Devi from Maddinayakahalli, Kolar“Incorporating biodigesters into our dairy farm has not only improved our milk production but has also lightened my workload. The time I used to spend managing waste is now spent on other productive activities, and the extra income has helped us reinvest in our farm. Seeing these benefits firsthand has made me an advocate for biodigesters among other women in our community.”

Kailashben from Gujarat“My life changed the day I started using the biodigester. My thumb was so damaged from gathering firewood every day that I couldn’t even register my fingerprint for Aadhaar. Since I started using the biodigester, my quality of life improved a lot. I don’t have to struggle to collect firewood anymore, and my wounds began to heal. I still have the scars on my hands, but they tell my story: one of resilience, change, and a future filled with hope.”

Conclusion

We must recognize that supporting regulatory frameworks, including microfinance policies and digital public infrastructure (DPI), as well as catalytic funding geared to increasing financing flows, help ensure that more fit-for-purpose credit reaches last-mile customers.

Reflecting on the project learnings, it is no surprise that access to relevant financing, mainly credit designed to serve smallholder farmers meaningfully, is the fuel to the engine. However, we must recognize that supporting regulatory frameworks, including microfinance policies and digital public infrastructure (DPI), as well as catalytic funding geared to increasing financing flows, help ensure that more fit-for-purpose credit reaches last-mile customers. These are vital in unlocking finance from formal financial institutions to serve the marginalized and the underserved.

While macro levers such as regulations were not a focus of this project, we touched upon a few nuances on the contrasting regulations in India and Kenya. More can be explored to identify successful and portable use cases that can be deployed across emerging markets, especially with the increasing conversations and focus of many economies on prioritizing DPI as a way to democratize data for the greater good.

Through project implementation, it was evident that the role of philanthropic catalytic funding is vital, and more of it is required to encourage formal financial service providers to service a new product (asset, insurance, etc.) and to go deeper into serving new-to-credit customers. Financial service providers are often tasked with a tricky balancing act of juggling portfolio quality and innovative product design. This dichotomy stems from regulations that mandate safeguarding against portfolio deterioration and financial markets that reward good portfolio quality by offering favorable rates for raising capital. Hence, financial service providers are inherently averse to serving the perceived high-risk segments such as smallholder farmers. In such scenarios, philanthropic catalytic funding plays a critical role in unlocking private capital through partnerships and driving system-level changes. This can be achieved by showcasing success stories that positively influence public sector regulatory and policy changes.

Through the project, we reached out to over 15 financial service providers across India and Kenya. Often, the willingness to participate in such innovative and exploratory business models was not an obstacle. However, due to policy and technology restrictions, the ability to be nimble in decision-making across the organization’s structures and agile in implementation demanded prolonged back-and-forth before partnerships could be formalized. Therefore, the time required for partnership formalization with financial service providers must be adequately accounted for in the project design. Upon partnership formalization, there are often aspects that require focused interventions that are uncovered through the gap analysis. For long-term sustainability and successful implementation, there must be preparedness to resource and plan for technical assistance interventions during the project design. Such interventions are catalytic in nature and enable financial service providers to push the envelope further in areas such as ecosystem partnerships, financial product development, and institutional and customer capacity building, whereby it would not be prioritized in the interest of catering to the day-to-day business needs.

Ecosystem partnerships enable financial service providers to better support women dairy farmers and promote inclusivity and economic empowerment. To address gender-specific challenges, financial institutions should move beyond collateral-based lending and leverage cash flow-based assessments or group guarantees tailored for women farmers. This is essential to accommodate women who lack land titles or formal credit histories. Field officers need gender-intentional training to combat unconscious biases and ensure women farmers are treated as primary decision-makers. Additionally, blended finance models and customized loan products tied to agricultural outputs can make adopting assets like biodigesters more accessible for women.

Financial service providers and their ecosystem partners should prioritize community-driven outreach, using local women’s groups to spread awareness about product benefits. Demonstration models at women-led farms and support for women-led producer organizations can further foster adoption. Marketing approaches must be gender-sensitive, featuring relatable success stories, while grievance redressal systems ensure women feel supported throughout the adoption process. These strategies will enable women farmers to overcome systemic barriers and achieve sustainable growth through green technologies like biodigesters.

Trust-building with financial service providers happens when you start within their comfort zone. Often, expectations are misplaced, and interventions and partnerships demand providers to serve a new product to a new segment that nudges them out of that comfort zone. For any new initiative targeting a new customer segment or product, financial service providers require the necessary internal approvals and operational set-up, which is vetted by the operations, risk, and business teams at a minimum. Consequently, project design should consider a runway duration that allows for the deepening of the relationship and trust-building. For example, it would be prudent to expect that an institution would be more comfortable launching a new product to its captive and vintaged customer base during pilots to understand the efficacy and risks of the product before extending it to a riskier segment as per their internal policies or to a new segment altogether.

It is important to note that credit risk instruments can help financial service providers avoid portfolio risk. While first-loss guarantees can cover monetary risk, having a lower-quality portfolio can have a more significant impact on the institution’s cost of borrowing capital because it directly affects its credit rating. Hence, internal policies and incentive structures are often aligned to ensure good portfolio quality and not necessarily encourage new products and services, which may be higher risk in comparison. Therefore, any approach that requires financial service providers to change their current operating model must be supported by incorporating organizational change management and institutional capacity building to ensure alignment and buy-in. Additionally, the internal policies and incentive structures must be altered to align with the project objectives, giving it the best chance of succeeding.

Also, given the current global food security challenges and the exacerbating influence of climate change, the immediate need is to scale targeted, affordable, and accessible solutions for smallholder farmers. While a lot of funding and investment commitments mandate scale, it may be remiss to ignore catalytic models that demonstrate new and innovative approaches to solving for access to finance to smallholder farmers, which has continually plagued global development. Funders, donors, and development finance institutions should not discourage such opportunities, as such projects and initiatives are the R&D labs for innovative models that have the potential to present new approaches that challenge the status quo.

Finally, but most importantly, the customer. Smallholder farmers operate from a position of trust and trade-offs. Through decades of trust erosion, from counterfeit fertilizers to digital payment frauds to overpromised and underdelivered subsidies, smallholders have become skeptical. Therefore, a one-size-fits-all approach needs to be replaced by meeting smallholders at their channel of comfort. This means looking deeper at each interaction and matching it to an adequate ‘trust’ channel. For example, introducing a new asset to women smallholders is better received in a group setting, compared to receiving a customer testimonial over WhatsApp. The customer decision-making lifecycle must be well understood and designed to address the nuances across gender, segments, culture, and seasonality.

Additionally, there is an abundance of innovation that can improve smallholder productivity and make them climate resilient. Access to finance is a massive hurdle for smallholders acquiring these technologies and assets. However, understanding the trade-offs is a precursor to the acquisition decision. There is often a dearth of knowledge that limits smallholders from making decisions that benefit them because the understanding of the short-term vs. long-term is often not clear. For example, while a biodigester may take three to four weeks to start generating utility in the form of biogas for cooking or energy, smallholders might hesitate to invest in it when they can use that money to buy more immediate inputs. Even if the benefits are clear, smallholders need a financing product that is patient and contextual, accounting for climatic events, family emergencies, market conditions, and others.

For smallholder farmers to succeed on the ground, a whole ecosystem needs to coordinate and collaborate.

Appendix

Impact measurement

To comprehensively assess product impact, we implemented a robust methodology combining quantitative and qualitative data collection approaches. We conducted a telephonic endline survey, reaching out to all customers and gathering 174 high-quality responses. This survey provided valuable numerical insights into customer satisfaction, usage patterns, benefits, and challenges. Additionally, we conducted detailed in-person discussions with 61 households, delving deeper into the specific benefits, challenges faced, and overall impact of biodigesters on their lives. These qualitative insights complemented the quantitative data, providing a holistic understanding of the product’s impact.

Customer profile

Since biodigesters are used at the household level, we engaged with entire households rather than just the owners. The demographic profile of customers is primarily based on the age of either the woman in the household using the biodigester or her spouse assisting with slurry management. Telephonic surveys were predominantly answered by men.

Awareness and decision-making in product adoption

Our assessment provided insights into how customers became aware of the product and their decision-making processes:

- Eighty percent of respondents were made aware of the product by Stellapps and Pahal staff through videos, pamphlets, and demo unit meetings.

- Twenty percent were introduced to the product through recommendations from friends and relatives.

- In face-to-face interviews, customers emphasized that the option to purchase the product in installments was pivotal in their decision-making. Stellapps customers appreciated the convenience of deducting EMIs directly from milk earnings, while Pahal customers found the Rs 25,000 ($295 USD) loan for additional costs highly beneficial.

- Visiting the demo unit was crucial for most customers and a key deciding factor for purchase. Many were initially deterred by perceived high costs or quality concerns, which the demo unit effectively addressed.

- Nearly all respondents suggested the demo unit visit and demo videos as the most effective ways to advertise the product. The Nukkad Natak (street plays) and product launch meeting had high recall rates, indicating effective awareness campaigns.

Role of financing

Accessible financing options played a crucial role in facilitating the installation of biogas units, making sustainable energy solutions affordable and accessible to women farmers.

By alleviating the financial burden of purchasing LPG, biogas units enabled customers to redirect savings towards incomegenerating activities, contributing to poverty alleviation (SDG 1).

Access to financing options

Customers universally appreciated the availability of financing for the asset. They acknowledged that without a financing option, the product would have been financially out of reach, even when subsidized. Many mentioned that after experiencing the product’s benefits, they would consider purchasing it without financing in hindsight. However, before their initial purchase, the availability of installment payments was a crucial factor in their decision-making process.

- During the endline survey, 32 percent of respondents indicated that they would not have purchased the asset if financing had not been available. In face-to-face interactions, when queried about a higher price range (approximately Rs 12,000 to Rs 15,000 [$142 USD to $177 USD]), most respondents emphasized the necessity of a financing option.

- Nearly all respondents, 99 percent, agreed that investing in productive assets is crucial for their livelihoods. Moreover, 76 percent responded positively to having the option to finance a new asset through installment payments, highlighting its perceived value and practicality in their financial planning.

Product impact on customers

We began the project with certain assumptions about the impact of biodigesters, all of which have been successfully realized:

- Financial independence: Customers experienced economic relief by saving on fuel costs, enabling them to invest in other household needs and income-generating activities. SDG 1 (No Poverty).

- Improved health: The transition to biogas led to a reduction in respiratory ailments and injuries associated with traditional cooking methods, enhancing the overall well-being of customers. SDG 3 (Good Health and Well-being) and SDG 7 (Affordable and Clean Energy).

- Gender equality: Women, who often bore the brunt of household chores, gained more autonomy and improved quality of life through the adoption of biogas. SDG 5 (Gender Equality).

Increase in Income

Improved quality of life

Regional insights

In Gujarat, customers noted that cooking bajra roti, which takes a lot of time, was previously expensive with LPG. With biogas, they can cook without worrying about the Cost, making their lives easier and more convenient.

Environmental impact

Biogas as a sustainable alternative can help reduce CO2 emissions and minimizes chemical fertilizer use:

With 250 biogas digesters installed, an estimated 1,500 ERs would be achieved every year, out of which 225 ERs are from replacing baseline fuels. “ER” stands for “emissions reduction,” defined by industry experts as one metric tonne of carbon dioxide equivalent that has been reduced, avoided, removed, or sequestered.

Net Promoter Score

The majority of customers asked would recommend the product to their friends and family.

Top 4 reasons for this high score are:

- quality of the product

- usability

- low cost

- easy finance option

Accion is a global nonprofit on a mission to create a fair and inclusive economy for the nearly two billion people who are failed by the global financial system. We develop and scale responsible digital financial solutions for small business owners, smallholder farmers, and women, so they can make informed decisions and improve their lives. Through targeted investment strategies, advisory solutions, and expert thought leadership, we work with local partners to develop and scale cheaper, more accessible, and customer-friendly financial solutions. Since 1961, Accion has helped build 267 financial service providers serving low-income clients in 75 countries, reaching 440 million people. More at accion.org.

All partner logos used with permission.

Published March 2025