We are living through a time of extreme difficulty — and that’s especially true for the world’s 3 billion people who are left out, or poorly served by, the global financial system. Without tools like savings, credit, or insurance, they are at risk of being left behind as we recover from COVID-19.

We are also living in a time of extraordinary innovation that is changing all our lives. This innovation has the power to solve complex problems at a critical time, and finally bring basic financial tools to those who need them most.

Innovation is chipping away old obstacles that surrounded the world’s poor. Today, no distance is too far, no transaction size is too small, and with data and data analytics, we can understand clients’ needs wherever they may live.

Early-stage fintechs are nimble, flexible, and digitally native — making them uniquely positioned to leverage technology and innovation for the benefit of vulnerable people and small businesses. Here’s how fintech startups in Accion Venture Lab’s portfolio are doing that:

- TerraMagna is using satellite imaging in Brazil to see small farms who are ignored by large banks. They use those images to assess collateral and figure out what a farmer needs to grow and thrive.

- Toffee Insurance has successfully reached India’s uninsured by offering “bite-sized” policies covering risks that are most relevant to consumers, like unexpected illness, bicycle damage, and theft.

- Field Intelligence uses AI and data analytics to help community pharmacies in Nigeria and Kenya optimize their inventories and ensure their customers have the medications they need, when they need them.

- Self is helping Americans with thin or damaged credit files build their credit scores through innovative credit-builder loans.

- CreditMantri is using alternative data sources to help consumers in India who have been invisible to the financial system access credit for the first time. (I recently had the honor of awarding Gowri Mukherjee, CEO of CreditMantri, with the 2020 Edward W. Claugus Award for leadership and innovation in financial inclusion.)

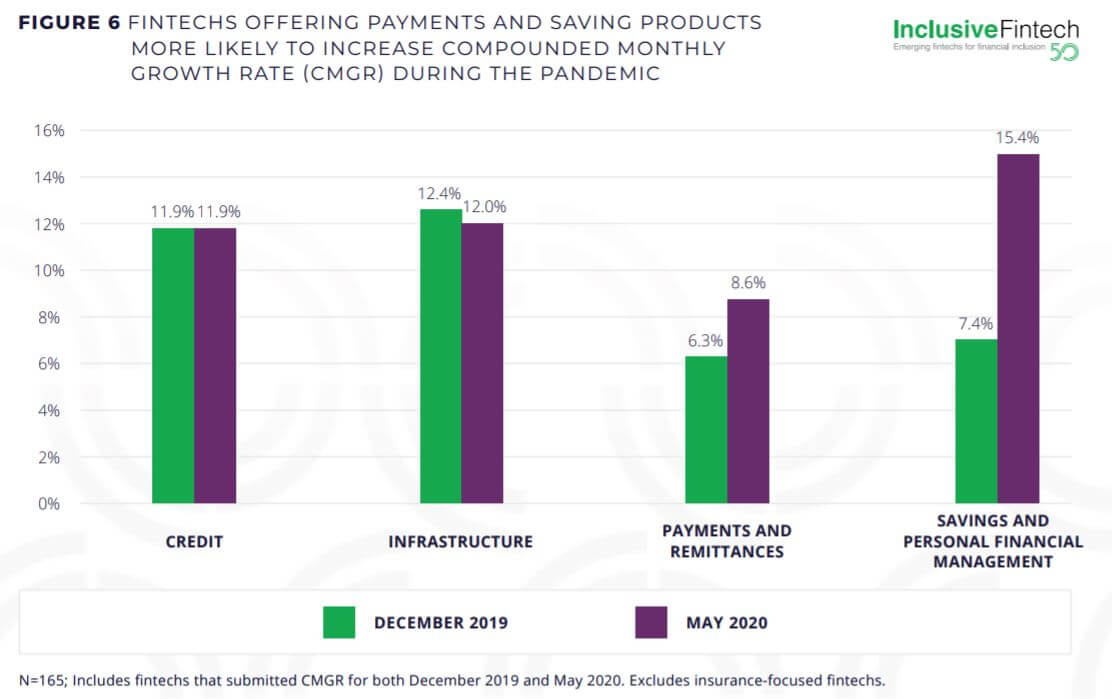

Fintechs are meeting customer needs during the pandemic

New data confirms how fintechs are answering new needs. In the initial months of the pandemic, consumer demand surged for financial products that build resilience, including savings accounts, personal financial management tools, and payment platforms. Fintechs offering these products saw their compounding monthly growth rate go from 7.4 percent to 15.4 percent from December 2019 to May 2020.

This insight comes from a recent whitepaper that looks at data submitted by the 2020 cohort of applicants for Inclusive Fintech 50, an initiative that elevates promising early-stage fintechs driving financial inclusion and resilience around the globe. The initiative provides valuable visibility, resources, and connections that startups need to grow and thrive, especially as they contend with the added problems raised by a global pandemic.

Fintechs must grow to continue supporting vulnerable people

Indeed, inclusive fintechs must overcome major challenges to grow, scale, and continue supporting underserved populations. In the midst of a global recession and limited funding, fintechs have had to extend their financial runways while simultaneously finding ways to grow their businesses.

To achieve growth quickly, historically, some fintechs have pursued a “grow at all costs” mentality that prioritizes customer acquisition. But customer acquisition can be costly: bringing on a new customer is anywhere from 5 to 25 times more expensive than retaining an existing one. Fintech startups should consider more sustainable pathways to growth, namely via increased usage, uptake, and earnings among existing clients.

We explore this concept in our latest publication from Accion Venture Lab that highlights how fintechs are doing just that. And building value for current users is very relevant in the era of COVID-19. Vulnerable people need more and new financial service innovations to rebuild their safety nets and livelihoods as their savings and inventories have been depleted.

I was also very glad to join two partners featured in the report, Jaime de los Angeles, CEO of Advance, and Tommy Yuwono, co-founder and director of Pintek at the Singaore Fintech Festival in early December. Pintek provides credit to students and schools to improve access to education in Indonesia—and has helped schools go online during the pandemic. Advance is a salary-on-demand platform that’s been adopted by large companies in the Philippines to provide employees with early access to their wages and promote financial wellbeing.

Inclusive fintech startups are offering inspiring examples of how innovation is answering today’s most urgent challenges. As we look toward building an inclusive recovery from COVID-19, we must ensure they have the tools and resources to grow sustainably and answer their clients’ most pressing needs.

Explore More